Recapping The Mission Plan

Mission Plan Series #5

moontower.ai has released a new series —> The Moontower Mission Plan

This guides a step-by-step progression for developing opinions on volatility which you can use whether you are trading options to bet on volatility itself, or more likely, to bet on direction.

An installment will be released once a week right here on substack.

If you want to access the entire Plan now, you can become a free member here.

We began this series with a set of principles to guide our action recipes.

In the Introduction To The Moontower Mission Plan, we learned:

Prices are a tangled mix of expectations and aggregate preferences.

The vol trader lens is agnostic on asset prices but axed on volatility.

You are likely axed on asset prices with your trades reflecting a mix of expectation and custom preferences or requirements.

The vol trader lens reveals the options that suit your needs.

When axes align: the overlap of your directional axis and volatility axis drives your option trades!

In Formulating Your Axe List, we learned:

Before you touch an option, you need an opinion about how its implied volatility is priced. Option prices are driven by variables besides just which way the stock moves.

You can step through the moontower funnel to populate an “Axe List” which broadly targets parts of the option surface for a set of names.

Your Axe List is a handy map whether you want to bet on direction with options (hedging/speculating) OR volatility directly (the most popular version of this is capturing the VRP).

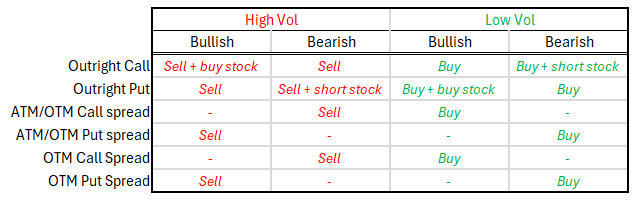

In Delta Mission: Volatility Meets Direction, we learned:

Professional vol traders are a sliver of capital markets. As an investor or trader, you most likely arrive at the moontower with a directional opinion on various assets and asset classes. Those opinions about which assets are buys, sells, holds, or ignores are downstream from your own research.

Equipped with your Axe List you now can match your directional view to your vol view.

Because of put-call parity, we can express any vol axe with bullish or bearish directional axe...and vice versa!

The general rule: Buy (sell) the OTM option in region of the surface you think is cheap (expensive).

In Vega & Theta Missions: Capture VRP (including covered calls/puts), we learned:

Structural risk premiums are compensate passive investors for patience and tolerating swings. Better performance is achievable for investors willing to put in work (although the noisy nature of markets doesn't guarantee effort will pay off -- sober but real).

We expect that selling covered calls or puts will be the most common ways users try to capture VRP. You are trading options around your own directional positions more intelligently by using your formulated vol axe rather than randomly selling calls against the assets you happen to own.

A smaller number of users will formulate an axe list without any directional bias. They will use the funnel to filter for option selling opportunities, strain the opportunities through a final discretion/context filter, and proceed with the trade.

The primary difference in approaches is the agnostic starts with a blank slate whereas the standard investor will check their directional axes against the vol funnel to see if there’s an option-selling opportunity on their short list of names.

Both approaches still occur in stages:

Identify the target & structure

Size the trade

Execute

Manage the position

Exit

See the original posts for details and references.