Mission Plan #3: Delta Mission -- Volatility Meets Direction

Mission Plan Series #3

moontower.ai has released a new series —> The Moontower Mission Plan

This guides a step-by-step progression for developing opinions on volatility which you can use whether you are trading options to bet on volatility itself, or more likely, to bet on direction.

An installment will be released once a week right here on substack.

If you want to access the entire Plan now, you can become a free member here.

In Formulating Your Axe List, we narrowed the options markets to a set of names and regions on their volatility surface that look cheap or expensive.

Take a breath. You did something few investors will ever do.

You are seeing like a vol trader. Like the Predator detecting heat signatures in the darkness.

It’s time to put these vol axes in service of our goals.

Directional Axes

From the introduction to this series:

Vol traders are axed in option prices but agnostic about underlying securities.

Investors are axed in securities but agnostic or even ignorant about volatility.

Professional vol traders are a sliver of capital markets. As an investor or trader, you most likely arrive at the moontower with a directional opinion on various assets and asset classes. Those opinions about which assets are buys, sells, holds, or ignores are downstream from your own research. Or if you’re like me, a healthy dose of “putting your finger in the air”.

But now, instead of being agnostic on option prices, you can align your directional axe with your newly discovered vol axes!

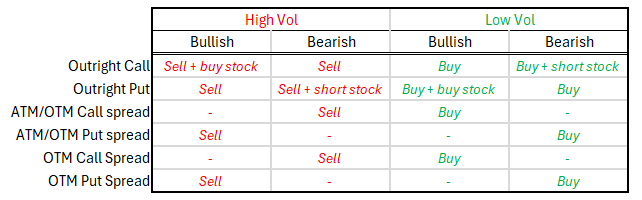

Expressing a bullish or bearish bet is as simple as:

buying/selling an outright call or put

buying/selling a call or put vertical spread

A few key observations:

1.Because of put-call parity an ITM call is equivalent to an OTM put.

You can mimic a long call position by buying the put on the same strike and the stock in a 1-to-1 ratio. This is why selling a covered OTM call is equivalent to selling an ITM put of the same strike

2. Buying a call spread is equivalent to selling a put spread of the same strikes.

Consider a $100 stock. If you buy the 100/105 call spread for $2 your maximum profit is $3 if the stock expires at $105 or higher. If you sold that same 105/100 put spread at $3, your maximum profit is also $3 if the stock expires $105 or higher.

These observations are powerful because it means:

We can express any vol axe with a bullish or bearish directional axe…and vice versa!

Let’s see how we can use the Axe List to construct directional bets.

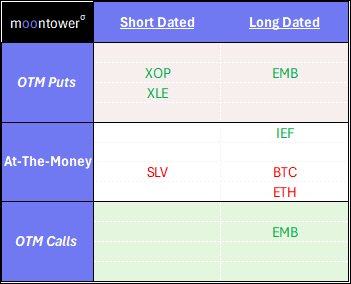

Our list from 4/9/2024:

The general rule:

Buy (sell) the OTM option in region of the surface you think is cheap (expensive).

This is simple but not necessarily intuitive. Let’s demonstrate using the above vol axes.

Examples

Diagnosis: cheap downside options

Candidates: XOP, XLE, EMB

Bullish expressions

Buy OTM puts AND the stock (or buy ITM calls)

Sell ATM/OTM put spread. You are buying the cheap region. This trade is more ambiguous because you are selling an ATM put and if you think the whole surface is cheap then this is not advised. ATM options have more vega than OTM options so being short such a put spread will be short vega and the put spread will hold or increase value if ATM vol increases.

Bearish expressions

Buy OTM puts outright

Buy OTM put spreads (ie 30d/10d put spread)

Diagnosis: cheap upside options

Candidates: EMB

Note the symmetry compared to the cheap downside diagnosis.

Bullish expressions

Buy OTM calls outright

Buy OTM call spreads (ie 30d/10d call spread)

Bearish expressions

Buy OTM calls AND short the stock (or buy ITM puts)

Sell ATM/OTM call spread. You are buying the cheap region. This trade is more ambiguous because you are selling an ATM call and if you think the whole surface is cheap then this is not advised. ATM options have more vega than OTM options so being short such a put spread will be short vega and the put spread will hold or increase value if ATM vol increases.

💡Notes on spreads

Spreads are less risky than outright trades. They have less vega since you are both long and short an option. If you trade spreads you can do the trades bigger than if you trade an outright option since the risk (and reward) is lower.

The further the distance between the strikes of a spread, the riskier the spread is. At an extreme width you are basically trading the nearer option like an outright. For example if you buy the 110-250 calls spread in a $100 stock.

Diagnosis: expensive downside or upside options

Candidates: None from our current vol axes

Still, let's explore the scenarios.

Expensive downside scenario

Bullish expressions

Sell OTM puts outright (notice that this is also a cash-secured put if you set aside the cash needed to buy the stock at the strike in the event of assignment instead of just posting margin)

Sell OTM put spreads (ie 30d/10d put spread)

Bearish expressions

Sell OTM puts and short the stock (or sell ITM calls). Note how this is the directionally flipped version of a selling covered calls!

Buy ATM/OTM put spread. You are selling the expensive region. This trade is more ambiguous because you are buying an ATM put and if you think the whole surface is expensive then this is not advised. ATM options have more vega than OTM options so being long such a put spread will be long vega and the put spread will fall in value if ATM vol subsides.

Expensive upside scenario

Bullish expressions

Covered calls —> Sell OTM calls and buy the stock (or sell ITM puts).

Buy ATM/OTM call spread. You are selling the expensive region. This trade is more ambiguous because you are buying an ATM call and if you think the whole surface is expensive then this is not advised. ATM options have more vega than OTM options so being long such a call spread will be long vega and the call spread will fall in value if ATM vol subsides.

Bearish expressions

Sell OTM calls. Of course, this is an unbounded risk.

Sell OTM call spreads (ie 30d/10d call spread)

Diagnosis: cheap ATM options

Candidates: IEF

Bullish expressions

Buy ATM calls outright

Buy ATM/OTM call spread. You are buying the cheap region and this is less ambiguous than spreads where the OTM option vol is cheap or expensive. Why? Because you are still long vega since you own the ATM option.

Bearish expressions

Buy ATM puts outright

Buy ATM/OTM put spread. You are buying the cheap region and this is less ambiguous than spreads where the OTM option vol is cheap or expensive. Why? Because you are still long vega since you own the ATM option.

Diagnosis: expensive ATM options

Candidates: SLV, BTC, ETH

Bullish expressions

Sell ATM puts outright. Much riskier than a spread.

Sell ATM/OTM put spread. You are selling the expensive region — this is less ambiguous than spreads where the OTM option vol is cheap or expensive. Why? Because you are still short vega since you are short the ATM option and time premium.

Bearish expressions

Sell ATM calls outright. Unbounded risk.

Sell ATM/OTM call spread. You are selling the expensive region — this is less ambiguous than spreads where the OTM option vol is cheap or expensive. Why? Because you are still short vega since you are short the ATM option and time premium.

The big takeaway is just shouting the general rule:

Buy (sell) the OTM option in the region of the surface you think is cheap (expensive).

If the vol is cheap or expensive, whether you are directionally bullish or bearish, there is a way to construct a trade to align your vol axe with your directional axe.

In the next chapter, Vega & Theta Mission, we will use the map for structuring volatility-driven trades such as capturing VRP (this will include covered calls/puts).