Friends,

Last week in Adam Smith’s Backdoor, I wrote:

The promise of capitalism is its swarm intelligence that maximizes benefit under the curve for the plurality of its members, as opposed to the narrow interests of a corruptible centralized authority.

If the “plurality of its members” see the gains as gilded with appeals to capitalism feeling like they are in service of capital instead of its citizens, then we are inviting the end of capitalism.

My worry was that capitalism contains the logic of its own destruction if we compress prosperity with a lossy “number-go-up” zip file. In defiance of “end of history” arguments a la Fukuyama, I suspect the romantic version of “capitalism” is an unstable, temporary condition. We’re lucky we got the run we did.

I left a teaser for today’s thought in last week’s note:

There is a technology woven into the very fabric of capitalism that, on a long enough timeline, inevitably exposes the backdoor.

The technology is an idea:

discounted present value

Like money, this is one of those ideas that we have become so acclimated to that we wouldn’t revisit its assumptions until we’ve abused the concept so thoroughly that its ability to bear weight is in question.

Current times have me questioning assumptions.

The traditional story

The logic of financialization says the value of everything can be made legible and denominated in some present value to be packaged, cut up, sold, and most conspicuously, borrowed against.

To do this, we must have both a sense of value and a framework for discounting that value. Both of these concepts are increasingly slippery in this age of abstraction and acceleration. The smartphone isn’t even old enough to drink, meanwhile, the annual capex of the top 4 firms chasing “intelligence” is a flow variable that rivals the capitalization of the most valuable company in the world 20 years ago.

A traditional story of company value rests on its earning power — the ability to marshall its assets into an output that is in demand to earn a margin. The margins, once they have recouped variable costs, financing costs, and restored the usefulness of the underlying assets (depreciation/amortization) can then be returned to the shareholder or re-invested. We can call that the leftovers. That the leftovers are re-invested can be thought of as a return of capital that is not under the investor’s control. It is part of their allocation but deployed like an SMA…the change in the price of the shares is a continuous referendum on whether this forward-looking decision is accretive or destructive.*

The return to the investor depends on the transfer of the leftovers to the equity owner. This transfer or bridge is safely suspended on girders of legal and tax assumptions. The legal assumptions are mostly captured in corporate governance statutes and enforcement practices. Tax is subject to government edict and enforcement practices.

Acceleration warps the story

Just as particle accelerators expose Newtonian assumptions, the acceleration we are living through challenges our assumptions. There is an astute section in this interview where Kyla talks of attention-as-capital, thus inverting the capital-driving attention dynamic. Attention used to be a tool to sell something of value. Now, attention itself is value.

Politicians, meme stocks, and coins internalize this feedback. Warning. I’m about to sound old-fashioned, but this development is bad news. In a world where attention is a means to an end — to sell something — there is a discipline baked into the loop. If the thing you sell doesn’t add value, the attention eventually dies on the vine. But what happens when the meta of attention is that we can profit from reflexively feeding it without any pretenses that there is a core of value underneath? When we don’t even bother with stories of utility in crypto and the product-market fit is gambling itself?

We’ve talked about the changing definition of “value” but what about discounting? A traditional framework for discounting is some blend of a “risk-free rate”, at least nominally guaranteed by the US government, and a margin to compensate for risk. The entire edifice of finance sits on a risk-free rate. CAPM, the risk-neutral replication of derivatives and insurance. Even FDIC insurance is an implicit RFR floor of zero.

An investor in an age of acceleration watches as commodity prices, real things, hover in familiar territory while “future cash flows discounted” reward attention — in some cases because of optimistic stories, in some cases because the company exchanges cash for BTC (an act which adds no economic value), and in some cases for nostalgic lolz.

Today, it’s embarrassing to think of actual value. The most basic form is stored energy**. An obvious example is oil. Slightly more abstract —a building is a collection of atoms that took energy to arrange and provides utility. It’s proof of work. Same with a good reputation. Then you look at Chamath raising another SPAC while everyone is in on the joke and you wonder if a bad reputation is even better than a good one? Is there any escape from this hall of mirrors?

How the growth imperative in this age of acceleration gives capitalism a bad name

Whatever this is, and I don’t really want to call it capitalism because I don’t want to give fuel to its undoing, but this “arrangement” that feels like capitalism taken to some post-modern, self-referential conclusion is at risk of sowing so much dissonance that it will invite an authoritarian savior if people can’t draw lines from having integrity, making real contributions, and a natural Dunbars law type of accountability to prosperity.

Financialization allows us to redistribute risk and, therefore, resources efficiently. But the idea is inherently leveraged to growth. That’s what drives the mark-to-market today. Society, which is asked to fend for its own retirement, cannot get in its way even if it has good reasons. It’s my fi-douche-iary argument or Matt Levine’s “everything is securities fraud” theme. Every claim is adjudicated through the lens of “Does this make my stock go up?” This is “discounted present value” as Frankenstein — a monster of our own creation, taking a life of its own.

Have we used the Frankenstein logic to allow attention-merchants to harvest escape-velocity levels of capital?

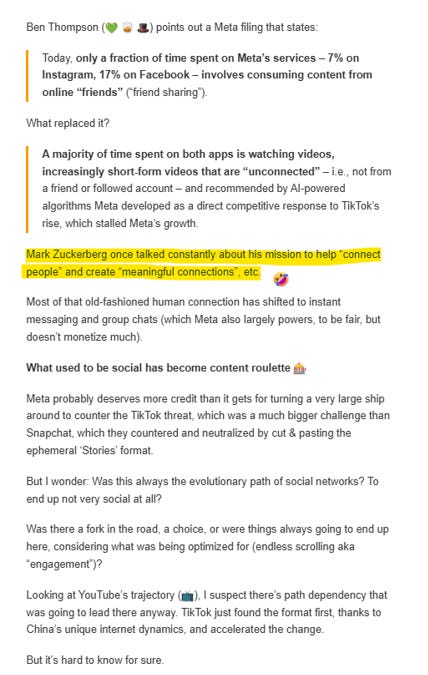

Consider Liberty’s blurb about the death of social networking (pardon my snarky highlight/emoji combo):

I non-ironically believe Zuck had to make this change to grow. When it comes to social media or maybe media broadly, the growth imperative means no good deed goes unpunished.

The amortization of future cash flows into a present value today predicated on growth is an idea that probably shouldn’t be extended to every type of corporation. Who would have imagined that you could gamble on sports on a futures exchange? The moment exchanges demutualized the growth imperative was in place. Betting is just the next green space.

In healthcare, one of the lesser-known but highly impactful provisions was the medical loss ratio (MLR) rule. It required health insurers to spend a minimum percentage of premium revenue directly on patient care and quality improvement, rather than on administrative costs or profit. Depending on the plan, it required 80-85% of the premium dollars to be spent on care. If insurers spent less than those thresholds, they were required to rebate the difference back to policyholders.

You see where this is going.

Since profit was effectively capped as a percentage of revenue (15–20%), the only way insurers could increase profits was by increasing top-line revenue (selling more policies or raising premiums). Not much incentive to cut costs when your profit is capped.

I’m not saying that we should treat health insurance, exchanges, and social media like utilities. But do we really want the growth imperative to be equally alive in all industries? If you poison society, but your market cap is fungible with lots of money then it’s not exactly crazy for someone to wonder about the relationship between value and money. If a BTC-treasury stock does meme its way into the SP500 where it will find itself in every retirement account in the U.S., our Frankenstein will turn anyone with a soul into the joker.

Let’s wind it down. It’s going to get weirder. Attention is a way to get rich by being a leech on society — now anyone can be an ambulance chaser. This weakens the link between value and prosperity. It weakens morale. Ultimately, capitalism is going to be the scapegoat. A lack of restraint ruining it for everyone else?

You can count on it.

Go get what’s yours.

*Random thought: Is there a foreign economy where the corporate sector has performed well (strong profits) but the returns have been underwhelming, disappointing, or possibly stolen? Is it possible that the assault on their bridges between corporate leftovers and investor returns can come to the American stock market…the American love affair with absentee ownership of assets in the form of corporate shares rests on that bridge.

**Increasingly think that a durable concept of a risk-free or least-risky rate is more likely to come from Vaclav Smil than U Chicago.

Stay groovy

☮️

Need help analyzing a business, investment or career decision?

Book a call with me.

It's $500 for 60 minutes. Let's work through your problem together. If you're not satisfied, you get a refund.

Let me know what you want to discuss and I’ll give you a straight answer on whether I can be helpful before we chat.

I started doing these in early 2022 by accident via inbound inquiries from readers. So I hung out a shingle through the Substack Meetings beta. You can see how I’ve helped others:

Moontower On The Web

📡All Moontower Meta Blog Posts

👤About Me

Specific Moontower Projects

🧀MoontowerMoney

👽MoontowerQuant

🌟Affirmations and North Stars

🧠Moontower Brain-Plug In

Curations

✒️Moontower’s Favorite Posts By Others

🔖Guides To Reading I Enjoyed

🛋️Investment Blogs I Read

📚Book Ideas for Kids

Fun

🎙️Moontower Music

🍸Moontower Cocktails

🎲Moontower Boardgaming