Ubiquiti Iniquity

Moontower Munchies #144

Friends,

When we renovated the fixer we bought in 2014 we installed wireless access points throughout the house. San Jose-based Ubiquiti made them. I haven’t heard of that company’s name again until I watched this insane story:

I’m on a total Pablo Torre kick these days. He’s a sports journalist who is leaning into investigative reporting. In this episode, he talks to one of the team members at Hunterbrook who broke the story about how Ubiquiti has been going around sanctions to supply Russian soldiers using the equipment to navigate battlefield drones.

When the story was published, Ubiquiti’s stock cratered (and since recovered much of the loss).

Quite the “U”:

Why is it a sport story? The founder of Ubiquiti is one of the richest (and youngest) NBA owners, Robert Pera. That the NBA cares more about Ja Morant’s transgressions than the Grizzlies owner seems about American as apple pie these days. A bonus fun part of the interview was the intro section where they talk about Pera challenging the NBA’s tenacious, no-chance-he'll-take-it-easy-on-you, “grindfather”, Tony Allen to a 1-on-1 game.

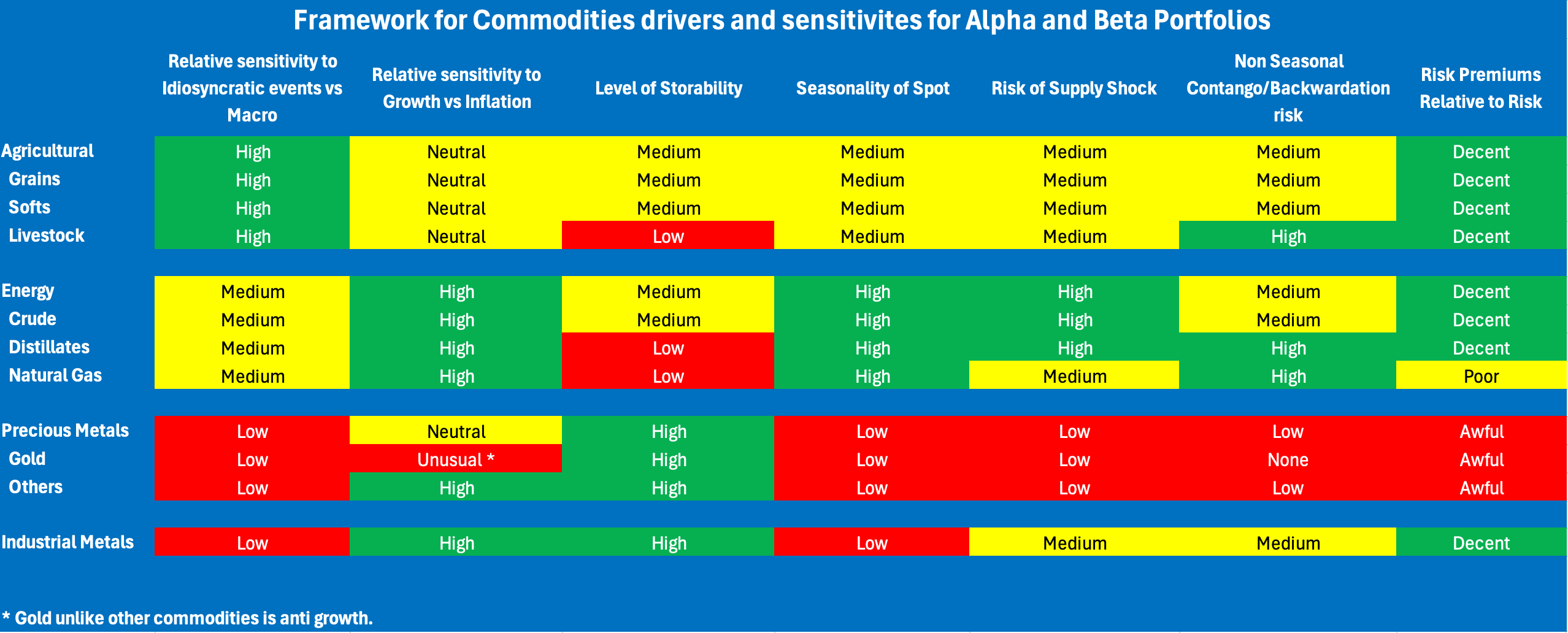

Commodities in an Investment Portfolio · 15 min read

A post I wish I wrote. Andy Costan’s post is part great story and part public service. The framework organizes commodity markets by their role, which in turn dictates what role they would play in an investment portfolio. I’ve thought about a lot of this in fragmented ways, but his synthesis is beautiful because it’s so damn clean.

Commodities have both spot and futures markets. In the short view, they are tasked with rationing demand through time, but a longer perspective, is they are the price signals informing investment in supply.

Spot markets have no intrinsic reason to have a risk premium. A futures market for the commodity might. He reasons through the factors that would inform the prospect of a premium such as convenience, storability, and liquidity. These factors drive hedging pressures.

My favorite part plays right into my general bias that “markets are hard to beat” captured in the post I re-published Monday:

Why You Don’t Get Paid For Diversifiable Risks

You could say the price of elegance is profit, but here’s the gist:

A truly great portfolio diversifier should have a lousy standalone Sharpe ratio. If gold reliably made you money in all environments, it would be too easy to own. Instead it gets bid until you are left a collectible with mediocre (or negative) risk premiums in exchange for the metal showing up precisely when your other assets don’t.

Most of the post is practical in that it teaches and sets your expectations for a passive/beta allocation. But he leaves room to discuss what I’d describe as the alpha surface of the commodity complex. Places for specialists to drill down:

In the name of reinforcement here’s another older post that explains why some assets will seemingly have prices that don’t make sense and why it often means you’re missing something:

Stay groovy

☮️

Need help analyzing a business, investment or career decision?

Book a call with me.

It's $500 for 60 minutes. Let's work through your problem together. If you're not satisfied, you get a refund.

Let me know what you want to discuss and I’ll give you a straight answer on whether I can be helpful before we chat.

I started doing these in early 2022 by accident via inbound inquiries from readers. So I hung out a shingle through the Substack Meetings beta. You can see how I’ve helped others:

Moontower On The Web

📡All Moontower Meta Blog Posts

👤About Me

Specific Moontower Projects

🧀MoontowerMoney

👽MoontowerQuant

🌟Affirmations and North Stars

🧠Moontower Brain-Plug In

Curations

✒️Moontower’s Favorite Posts By Others

🔖Guides To Reading I Enjoyed

🤖Resources to Get More Out of AI

🛋️Investment Blogs I Read

📚Book Ideas for Kids

Fun

🎙️Moontower Music

🍸Moontower Cocktails

🎲Moontower Boardgaming

Hi Kris, How are you measuring the risk premium of gold? and then relative to risk? what are the components of that? Thanks for the great work.