Perspectives On Values, Needs, Liquidity and Aging

Moontower #175

Friends,

Welcome to year 4 of this party at the Moontower. I took a 3 week holiday break from writing and the universe sent locusts. Well, a different bug at least — Covid and RSV which I’m pretty sure is bronchitis rebranded from the 1980s when I was a kid. Our house was a petri dish and the rain has been non-stop, although as a Californian you’re not allowed to mention precipitation without the solemn acknowledgment “we really need it”. I’m inside playing a lot of NBA2k23 with the kids and as much fun as that is, I’m done with winter. But like Pepé Le Pew, I doubt it’s done with me. Bah.

One silver lining was doing stuff I don’t do as much as I would sometimes like to — play guitar (1,2,3 songs with friends), watch movies (Bardo stood out) and binge TV (Classic Concentration reruns). I watched some mainstream stuff too. Avatar 2 and…White Lotus season 2.

I enjoyed and would recommend season 2 (I haven’t seen season 1 but it’s not necessary). White Lotus is a murder mystery but the mystery is actually not central to the show. The characters and dialogue are the draw. I recently watched this ancient but outstanding interview with Tarantino where he contrasts how American cinema [used to be] best at storytelling while “Europe was where you had character-based or mood-based films”. (Eddie Izzard’s old bit about British vs US movies implants the distinction with the stickiest mind-adhesive — side-splitting laughter). White Lotus is more in the spirit of a European film with a cheap Coen Brothers-style plot pushing the series forward.

The scenery in Italy is a timeless luxury. The acting is exceptional. Sure, the references to “mimetic desire” and “dark triad” felt focus-grouped from Twitter but it totally works even as a nod to the terminally online. The show provoked a lot of thoughts that I expected would have been covered in reviews. I don’t normally read reviews until after I watch something so I can see how my interpretation squares with English majors with much better literary comprehension skills than I do. In this rare case, I found the quality of reviews to be unsatisfying, lacking the depth clenching the show. (If anyone has a review probably from a Substack that stood out pass it on…I’m too lazy to write one myself because it would require a second watch. It’s a weak-sauce excuse. I’m torn between saying “sorry” and “tough”).

The editorial The White Lotus Nails How We Struggle To Reassess Classic Cinema does an admirable job of covering one of the show’s remarkable repartees:

Grandpa Bert Di Grasso planned the trip to get in touch with the family's Sicilian roots, including worshipping at the altar of "The Godfather." He lights up with absolute glee when telling Portia why their lunch location is so important, reveling in how Al Pacino cries out "Apollonia!" as the Corleone character watches his wife explode before his eyes. "It's a great scene," Bert declares. Portia, having zero nostalgia or cultural kinship to the film pushes back. "She blows up? Like, blows up? It's a little tasteless maybe," she says.

Bert immediately tries to double down by saying, "Well, look, they're trying to make a buck. They own the house where they shot the best American movie ever made," but Portia finds a (possible incel) softboi ally in grandson Albie, who confidently disagrees with his grandpa about the film's brilliance, telling him he only likes it because:

"you're nostalgic for the solid days of the patriarchy…men love 'The Godfather' because they feel emasculated by modern society. It's a fantasy about a time when they could go out and solve all their problems with violence and sleep with every woman and then come home to their wife who doesn't ask them any questions and makes them pasta."

My favorite part of the scene is the chicken-egg tension that follows:

Bert and Dom Di Grasso then go on to say that "The Godfather" is a "normal male fantasy," which Albie disagrees with and instead says, "No, movies like that socialize men into having that fantasy." His father pushes back: "Movies like that exist because men already do have that fantasy. They're hard-wired," and Bert agrees. "Mm-hmm, comes with the testosterone." Albie can't let it go, and either because he genuinely believes what he's saying or because he's trying to impress Portia by coming off as "one of the good ones," he declares, "No. Gender is a construct. It's created."

The article continues…

The scene is magnificent because it's a circle of three generations of men being so loudly wrong about the message of "The Godfather," while simultaneously nailing why conversations surrounding classic films are never-ending and consistently complicated. All three of the Di Grasso men were introduced to "The Godfather" in different eras, and their relationships to masculinity are completely different because of not only the changing social climate, but the types of masculinity modeled for them by the men in their lives.

The interpretation of historical figures through contemporary values is a guaranteed click-bonanza as people who think they can anticipate “the right side of history” battle with those who take an unnecessary apology so far that they come out the other side of the Pac-Man map needing to actually apologize.

The scene ends with a line that could have been captioned with “to be continued all-the-time and forever on the internet”:

"They used to respect the old. Now we're just reminders of an offensive past."

Does the Godfather’s masculinity reflect or culturally manufacture our apparent nature? I hate the trading advice if you don’t know what to do “sell half”, but I feel like bi-directional causation is embedded in so many forms of expression that any broad concept that devolves into a nature/nurture argument is hard to lay long odds on.

My “sell half” cop-out in this particular example is to recognize that men's physical dominance is a thing but that it explains many behaviors rather than justifies them. “Explains but does not justify” is a phrase I picked up from Russ Roberts’ Do I Deserve What I Have Series which I reference in Why ‘Deserve” Makes My Skin Crawl. Russ asserts:

Accomplishments explain results; they don’t justify them

Explanations are not justifications anymore than temptations determine outcomes. There’s a layer of personal agency that resides between eating a pint of Salt & Straw every day and not fitting in your jeans. Id vs ego.

Collectively, there’s a layer of cultural agency. Impulse vs laws. We like, decide, about stuff.

Decisions are never justified “just because [insert banal observation about nature]”. Discussion and debate are part logic, but that’s still only downstream from our value weightings. And those weightings can’t always be reconciled. In fact, if you take the wide-angle view of the human experience, it’s a miracle that we can agree enough to have any kind of general order. I have Oliver Sacks’ 1985 book The Man Who Mistook His Wife for a Hat and Other Clinical Tales on my nightstand. It’s a reminder that our perceptions and values are widely different cross-sectionally. This short post When Childhood Was Discovered explains that childhood as a concept is a fairly modern idea. It’s pretty clear that despite 23 pairs of chromosomes being a common denominator throughout history, we, as in the anthropological “we” change much faster than the 8th-grade life science “we”.

Arguments that pretend otherwise, leaning their full bodyweight on one side of the nature/nurture divide, collapse as soon as a second perspective enters the room. If the internet “dress” from 2015 taught us anything, it’s that we don’t even perceive colors the same. Good luck with the Godfather.

Money Angle

I have a friend who turned $2k into $6.5mm, eventually cashing out of the crypto markets with about $2.5mm. Because of the path, his framing is “what could I have done better?” He came to me looking for perspective on risk management.

I began my reply with a story I recounted in Talking To The Diamond Hands. In 2017, I was at dinner with a young product manager at Coinbase and an older tradfi friend that brought us all together.

At some point, the product manager who was about 22 went to the restroom. The senior guy, in a hushed tone, turned to me.

“So one of the reasons [the 22-year-old] wanted to talk to you is he has a high-class problem. He’s sitting on a giant pile of ETH he’s been mining since college. At current prices, he’s rich, but doesn’t know anything about investing. He needs advice and we thought you could help.”As I was soaking that it in, our young tycoon was returning. There was no need to tippy-toe. The whiz kid cut right to it. He explained respectfully and with great maturity his “problem”.

What did I say to him?

“I don’t have much to say. If you listened to my opinion years ago you would never be in this beautiful predicament. I would never have held on this long, so there is nothing I can say that you should listen to. But now that you are here, I can offer one way to think about it — sell an amount that makes you feel like you never have to take a job just for money. You are 22 and achieved freedom.”

I don’t even know if this is good advice. It feels like such a dowdy perspective that it can only come from someone who would never have scored that big.

I re-told this story because I wanted to highlight an important point — there is no risk management rule forged from the business of trading that condones having most of your eggs in one basket. In other words, there’s no vetted risk management framework that would have let you turn $2k into $6mm so the entire conceit of “what could I have done better?” is misplaced.

That doesn’t mean it was wrong necessarily. It depends on your goals.

If you need ransom money by Friday, not betting everything on a roulette wheel tomorrow might be the riskiest course of action.

I’ve explained how bet sizing is not intuitive. I’m reading a Man For All Markets now, and there’s a scene where a 38-year-old Richard Feynman explains to Ed Thorp how he agreed to “be the house” for another friend who wanted to play roulette. Playing as the house, Feynman taps out after losing $80, underestimating the short-run variance of the game despite his advantage. The Nobel Laureate’s failed gambling intuition cautions us mortals that in some areas you should “work out the math”.

Now notice that my friend’s pickle is really not even at the level of bet sizing where we can triangulate on a reasonable range of answers given some constraints. My buddy’s dilemma is philosophical. What are constraints and the goals? His first task is to back up and find the inputs that reduce to “what matters to me”.

It reminded me of another conversation with a family member who was trying to solve what I’d call a “thymos-question” with a spreadsheet. Look, if you have a high income but feel the burning call to press your full potential in something that is just not lucrative, Excel isn’t going to help. You can’t generate a 3-D chart with a binary z-axis labeled “living the one life I got” and “dead”.

Luck is not a strategy. But it exists. If you want to bet on variance maybe the most practical thing to remember is “trade less when you don’t have an edge”. You are in the exact mirror situation of a casino with a small edge that wants you to pull the handle every day.

Once you know you’re gambling and decide that even long odds are the only acceptable way forward, try to minimize your contact with the rake, and shoot your shot.

Money Angle For Masochists

All option traders have stories about days they regret going into the office because they had a massively winning option position that they mitigated by hedging too aggressively. A $1 OTM put that goes $10 ITM, but they bought stock the whole way down hedging the delta. Or a short straddle that pins on expiration but the stock’s daily range meant they bought the high and sold the low. In the long option case, liquidity was the enemy — you would have preferred the stock gapped down $10.

Think now what this means for options backtests that pretend closing prices are the only prices. Your sampling frequency should align with the frequency by which your p/l matters. If you sample daily but your intraday risk and p/l matter you are acting like an ostrich.

This observation is rarely overlooked in short option strategies, at least by non-charlatans, but it’s worth noting that long options strategies that over-index on gapping price charts will overstate their attractiveness since the gaps are a gift in “not being able to rebalance”.

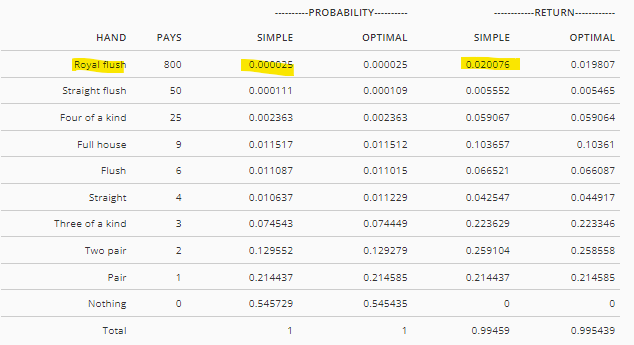

Since long option p/l’s can have highly skewed distributions (ie most of the profits coming from a few trades) this is not just a theoretical concern. Consider the expected value computation for optimal video poker play:

The Royal Flush, an event that happens 1 in 40,000 hands (if you played a hand every 10 seconds and didn’t sleep from Monday to Friday you’d expect to get one Royal Flush) contributes 2% of the game’s return. Said differently, if there was no possibility of a Royal Flush the house edge goes from .5% to 2.5%. This would be like the bid-ask spread in a $10 stock going from a nickel to a quarter. Annualize that churn in any strategy and see what happens to the “alpha”.

There’s a Wario world perspective (cc private equity) in which the downside of illiquidity gets moral equivalence with its upside. If you can’t re-balance you are safe from yourself and behavioral trading biases. Like pretending that every gap comes back. That’s the unsaid assumption that discourages you from selling at in-between prices. (If close-to-close vol is much lower than OHLC or tick vol then you want to sell straddles and go on vacation. Basically betting on mean reversion. Too bad this volatility behavior is only known in hindsight. Conversely, if you are long gamma you want to hedge more frequently if you know that close-to-close vol computations are smaller than range or tick vol computations of realized vol. If only you could know in advance.)

Well, this week Matt Levine wrote a banger called Structure. First an echo:

One cynical way to understand private investing generally is that private investment firms — venture capital, private equity, private real estate, etc. — charge their customers high fees for the service of avoiding the visible volatility of public markets. If you invest in stocks, sometimes they go up, and other times they go down. If you invest in private assets, they don’t trade; sometimes they go up (because companies raise new rounds of capital at higher prices), but the companies and the investment managers take pains to keep them from going down. This makes the chart of returns look much nicer — it mostly goes up smoothly — so the private investment managers can charge higher fees. We talk about this theory from time to time around here.

The real meat of the post is describing how start-ups, rather than taking a down-round in funding, prefer “structure”. Levine walks through the mechanics, but the gist is that the new investors who subscribe at the stale, overpriced valuation are getting an embedded put option (it’s more of a put spread since it only protects you so far). This gives the illusion that the valuation is unchanged, but only because you didn’t assign the put value. If you wanted to compare valuations over time, you’d need to back out the value of the put, to see how much the private company’s value has actually fallen.

Instead, we are left with the optics that the valuation is the same but the economic reality is that it’s lower. That should tell you quite a bit about the dog-and-pony culture around private investing. (In fairness, Levine explains how most insiders understand all this but that makes the gaslighting even darker in my axiological naivety).

I’d accept the pushback that it’s all made up anyway so who cares if we decompose the price of the glitter from the measure of fairy dust.

Last Call

Martin Shkreli Explains Why Sam Bankman-Fried Got Lucky With His Judge (80 min)

One of the YT comments says it best: This episode was fascinating. Martin is an amazing narrator. Like the David Attenborough of prison.

Martin loves to talk. It’s surreal how much he tells us.

My friend Khe is hosting a free 3-day free event called Your Roadmap for an Epic 2023. The only disclosure I have for promoting this is that Khe is a damn ninja. If you need help unlocking this is your jam. It starts January 10th.

Sign up hereWhat to expect:

Day 1: A Productivity System that Works For You

Day 2: Find Your Focus and Achieve Clarity with “Radical Prioritization”

Day 3: The 20-Minute Productivity Plan

From My Actual Life

New Years’ energy comes with resolutions. I deleted the Twitter app on my phone. Using it on my desktop only has cut my usage dramatically. I don’t know how much free time this creates but I’d be embarrassed to admit it even if I did. Better late than never.

I’m combining this resolution with another: write or work on writing projects for 2 hours a day. (In addition to an essay backlog, I have 6-8 writing projects in various stages of progress. They lean towards being guides/educational wikis.)

Being more explicit about this is a personal necessity. The more I get done in the general (if still poorly defined) pull of my ambition the better I feel. For better or worse, this is my wiring. I probably only love myself conditionally. I’ll deal with the fallout of that one day, but today’s not that day. Writing feels like a large component of that — it’s best to give imposter syndrome the finger once and for all.

Part of the productivity kick is checkboxing daily fitness, even if it’s just an hour’s walk, and reading books or technical material. My goal is an hour a day there, and reading substacks and articles doesn’t count towards that goal. I have about 70 books on my nightstand that I want to read and need to build that muscle again. Plus it’s a critical complement to improving my writing.

Separately, I’ve used also turned these projects into stand-alone websites:

The Moontower Volatility Wiki —> https://moontowerquant.com/

The Moontower Money Wiki —> https://moontowermoney.com/

These will continue to see progress. In addition, I will be rolling out another website that is a bit of a learning wiki. As I work on projects related to education/teaching/learning that site will be a companion where I will share stuff I learn in public. It will be a living document. Open source ethos and all that. I’ll share it in this letter when I publish it.

I’ll wrap with this:

We watched the Chris Hemsworth Limitless series on Disney+. Chris basically works with a different personal wellness expert in each episode to learn about stress, brain health, physical performance, and increasing your healthspan not just lifespan. It’s educational and often poignant. Australia is also shot beautifully. Eye candy. So is Chris (dudes you know it’s true too). Thor also seems shockingly down-to-earth.

There’s a scene in the death episode where he asks a stage 4 cancer patient in her 20s what she thinks about aging. Her response is pure perspective:

Aging is beautiful. I’d love to age.

Let’s have a groovy 2023, thanks for coming along!

Substack Meetings

I was invited to be a part of the Substack Meetings beta. You can book a time to chat. I’m more expensive than a 900 number from 1988 and have a less sexy voice.

Book a meeting with Kris Abdelmessih

Moontower On The Web

📡All Moontower Meta Blog Posts

🧀MoontowerMoney

👽MoontowerQuant

🌟Affirmations and North Stars

✒️Moontower’s Favorite Posts By Others

🔖Guides To Reading I Loved

📚Book Ideas for Kids

🎙️Moontower Music

🍸Moontower Cocktails

Becoming a patron

The Moontower letter is and will always be free. My writing is a search “for the others”. The “others” are people like you who are unlearning the mental frames that artificially narrow our choices.

If you are here you already understand that inspiration is a tradable good. It’s not as tangible as a cup of coffee, but it packs 10x the adrenaline with an infinitely longer half-life than caffeine.

If you feel inspired, you can upgrade to becoming a patron.

Lovely essay. A short note on the structure in private cos point. Because private companies only have price discovery on occasional points, it is simultaneously aiming for a future value, not optimising present day. Without a liquid stock companies optimise for storytelling (future value), employee recruitment and retention (options have a strike price), and ensuring momentum. A downround often makes mathematical sense, but it also creates a negative spiral for these companies, a lot of which are basically being built on hope anyway. Not meaning that negatively, they're literally building things that don't exist yet.

Trading with an edge is a helpful frame as is the counter.

Doing a blocking of apps and such too. Just paid for freedom which was $75 for lifetime. Loving it so far