Well What Did You "Expect"?

Moontower #179

Friends,

I’ll be brief up top today because both Money Angles are long.

In Wednesday’s Munchies I linked to Notes From Your Move (What Boardgames Teach Us About Life)

I forgot one fun bit Joan Moriarty wrote in the book:

At family gatherings, my father's relatives used to play [a game] called Fictionary. One player would take a dictionary, open it to a random page, find a word none of the players knew (this might take a couple of tries) and then write down the definition. The other players would each invent a phony definition for the word, write those down, and pass them to the player with the dictionary. Then, one at a time and in a random order, all the definitions, real and fake, would be read aloud. On the second reading, the players would try to guess which was the real definition. They would score one point for guessing correctly, and one point for each other player who was tricked into that their phony definition was the real one.

Party game fans will feel deja vu. This is the game Balderdash.

Joan makes a comment in the book about how sometimes a clever entrepreneur can get people to pay for something that is actually available for free. I love the game Decrypto but it’s also a game that you could play for free. Unlike Balderdash, the game components and art are actually pretty cool. Take my $20 please.

I do have fond memories of playing Balderdash with a group of NYC friends back in the day. My friend Ben had written a couple amazing answers that I kept in my wallet for many years until the ink finally bled off the slips of paper. One twist we added is to keep a spreadsheet where you log who voted for who’s answer every round. We liked seeing if certain people were susceptible to another player’s specific writing style.

I think my friend Lukshmi had me pretty dialed in.

Anyway, go play some games.

Well read about money first, then go play some games…

Today’s letter is brought to you by the team at Ezra:

Ezra is on a mission to make cancer screening available to everyone.

Studies show that for most cancers, survival at one and five years is much higher if the cancer is detected early (at stage 1) than if it is detected later.

Ezra screenings detect signs of potential cancer and other diseases in up to 13 organs in under one hour. The process starts when you create an account and choose a time and location that works best for you. By partnering with the best imaging centers and radiologists across the country, Ezra provides a reliable, seamless experience. After your screening, your Ezra clinician takes you through your easy-to-interpret Ezra report and any actionable next steps.

Moontower readers can get a $150 discount off of any Ezra full-body screening by using the code MOONTOWER150 at checkout or $50 off of a Low-Dose CT Scan, which screens for lung health, with the code MOONTOWER50.

Visit ezra.com to learn more.

Money Angle

Here’s a simple coin flip game. It costs $1 to play.

Heads: you get paid an additional $1 (ie 100% return)

Tails: you lose $.90

The expectancy of the game is $.05 or 5%.

We compute expectancy:

.5 * $1.00 + .5 * (-$.90)

It’s exactly the same calculation as a weighted average or arithmetic mean. This is a useful computation for many simple one-off decisions. Like should I buy an airline ticket for $1000 or the refundable fare for $1,100?

If there’s a 10% chance I need a refund then the extra $100 saves me $1,100.

10% * $1,100 =$110 which is greater than the $100 surcharge. 9% is my breakeven probability.

It’s tempting to use this logic in investing. Let’s say you expect the stock market to return 7% per year on average for 40 years. Start with $100 and plug in numbers:

$100 * 1.07⁴⁰ = $1497

Yay, you expect to have about 15x your starting capital after 40 years!

Eh. Sort of.

See the word “expect” in math terms and in colloquial terms is a bit different.

If I bet $1 on that coin game I theoretically expect to have $1.05 after 1 trial. In reality, I’m either going to end up with $2 when I double up or $.10 when I lose.

Another example:

I roll a die. If it comes up “1”, I win $600. Otherwise, nothing happens. Theoretically, I expect to win $100:

1/6 * $600 + 5/6 * $0 = $100

But if I asked you what you “expect” to happen if you play this game…you “expect” to win nothing. You only win 1/6 of the time after all.

Back to the investing example.

Investing is not a one-off game. It’s a compounding game where you plow your total capital back into the sausage machine to get that 7%

That’s why we use 1.07⁴⁰.

You are counting on your $100 growing by 1.07 * 1.07 * 1.07…

So that 15x number…that’s mathematical expectancy the same way the dice game is worth $100 or the coin game is worth $1.05 even though those outcomes are never actually experienced.

What you expect to happen in the colloquial sense of the term is the geometric mean. The arithmetic average is a measure of centrality when you sum the results and divide by the number of results. (In our examples you are summing results weighted by their probabilities, but you are still summing). The geometric mean corresponds to the median result of a compounding process. Compounding means “multiplying not summing”. The median is the measure that maps to our colloquial use of “expected” because it’s the 50/50 point of the distribution. That’s the number you plan life around.

The theoretical arithmetic mean result of playing the lotto might be losing 50% of your $2 Powerball ticket (which is another way of saying you are paying 2x what the ticket is mathematically worth). The median result is you lit your cash on fire. You plan your life around the median, especially when it’s far away from the mean. We’ll come back to that.

With investing we are multiplying our results from one year to the next together. The geometric mean is what you actually “expect” in the colloquial sense of the term. The geometric mean is more familiarly known as the CAGR or ‘compound annual growth rate’.

What is the relationship between the arithmetic mean to the geometric mean? This is the same exact question as “what is the relationship of mathematical expectancy and the CAGR?”

It’s an important question since that theoretical arithmetic mean is only expected if we live thousands of lives (actually there are ways to experience the arithmetic mean without relying on reincarnation. This is pleasant news because what good is being rich if you come back a pony.) We want to focus on the CAGR, which is much closer to what we might experience.

It turns out that number is lower.

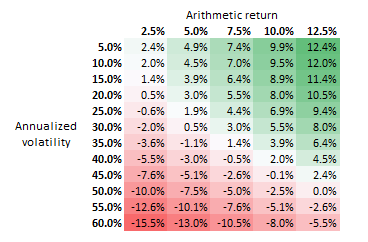

How much lower? It depends on how volatile the investment is. The formula that relates the arithmetic mean and CAGR:

where:

σ = annualized volatility

If an investment earned 7% per year with a standard deviation(ie volatility) of 20% you can estimate the CAGR as follows:

CAGR = .07% - .5 * .20² = .05

In arithmetic expectancy, over 40 years you expect to earn 1.07⁴⁰ = 15. You expect to have 15x’d your money.

But the median outcome, which corresponds to the geometric mean is 1.05⁴⁰ = 7.

7x is much closer to what you “expect” in the colloquial sense of the term. Less than 1/2 the arithmetic expectation!

The formula tells us that the arithmetic and geometric mean (“CAGR”) will diverge by the volatility. And that volatility term is squared…which means the divergence is extremely sensitive to the volatility.

This is a table of CAGRs where you can see the destructive power of volatility:

Why is volatility so impactful on a compounded return?

An easy way to see the impact of high volatility is to imagine making 50% and losing 50%. The order doesn’t matter. You have net lost 25% of your initial capital.

We can compute the geometric mean by weighting each possibility by its frequency in the exponent (in this case the exponents must sum to 2 because that’s the sample space — up and down):

.5¹ x 1.5¹ = .75

Go back to the first game in the post. You invest $1 in a coin game. Heads to make 100%, tails you lose 90%. This game had a positive arithmetic expectancy of 5%.

What is our arithmetic expectancy if you compound (ie re-invest) by playing 2x then the total possibilities are:

HT: 2 x .1 = .2

HH: 2 x 2 = 4

TH: .1 x 2 = .2

TT: .1 x .1 = .01

Since each scenario is equally likely (25% each) the arithmetic expectancy is simply the average = 1.1025

This jives with 1.05² = 1.1025

The average arithmetic return compounds as expected.

But our lived (median) experience is much worse. The median result is .20, a loss of 80%!

We could have seen that by computing the geometric mean:

2¹ x .1¹ = .20

Driving the point home with an extreme example

Consider a super favorable bet.

You roll a die:

Any number except a ‘6’: 10x your bet

Roll a ‘6’: Lose your entire bet

The arithmetic expectancy is ridiculous.

5/6 x 10 + 1/6 x -1 = 8.167 or ~700% return

But if you keep reinvesting your proceeds in this bet, you will go bust as soon as the 6 comes up. The median experience is a total loss, even though the arithmetic expectancy compounded is wildly positive. If you played this game 20 times in a row you’d [arithmetically] expect to make ~ 700%²⁰.

But you have a 97.4% chance of going broke because you need “not a 6” to come up 20 times in a row = 1 - (5/6)²⁰

That arithmetic expectancy of ~ 700%²⁰ is being driven by the single scenario where the 6 never comes up (that occurs 2.6% of the time). In that case, your p/l is $10²⁰ or between a quintillion and sextillion dollars.

But the geometric mean is 0 because multiplying over the 6 sample spaces:

10⁵ x 0¹ = 0

I chose such extreme examples because nothing illustrates volatility like all-or-nothing bets. The intuition you need to keep is that high volatility means you should expect to lose your money even if the arithmetic expectancy is high.

As soon as you start re-investing (ie compounding) your results are going to be governed by that geometric mean which hates volatility.

For the people who tout lotto ticket investments like crypto or transformative technologies with talks of “asymmetrical upside” or “super positive expectancy” remember even if they might be right, the most likely scenario is they lose all their money on that investment. Even literal lotto tickets can tip into positive expectancy. When that happens how much do you put into it?

Exactly. Not much. Because you know what to expect.

The role of rebalancing and diversification

Investing is not a one-off game. You always re-invest. By re-balancing, you “create” more lives by not concentrating your wealth in a single bucket which swamps the rest of your portfolio as it grows. If you never rebalanced BTC on the way up it would have eventually become nearly 100% of your portfolio and then 2022 happened.

If you don’t ever rebalance you are effectively praying that “not a 6” comes up for the 40 years you are compounding wealth. It’s not as extreme as that because market volatility isn’t as extreme as dice or coins. But the principle holds.

You only get one life so you care about the median. Diversification plus rebalancing gives you the god-perspective of getting to invest a fraction of your wealth into many lives.

Keep in mind — rebalancing is not changing your overall expectancy; it's changing the distribution of returns by pushing the median return (geometric mean or CAGR) up to your theoretical arithmetic return. This trade-off is not free. If you rebalance you don’t get the 1000x payoff that occurs when a single concentrated position hits 50 heads in a row.

Money Angle For Masochists

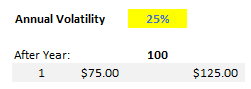

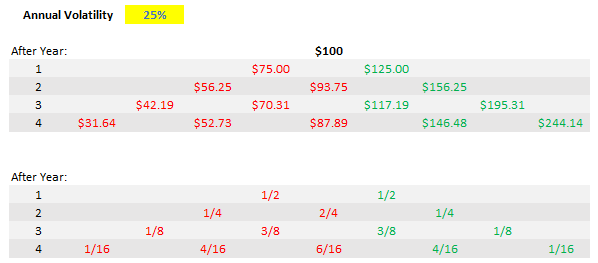

Imagine a $100 stock that can either go up or down 25% every year.

It’s 50/50 to be up or down.

Let’s look at the distribution of the stock after 4 years (with the probabilities of each price below it)

Look at the extremes after 4 years:

$31.64

A -25% CAGR over 4 years = cumulative loss of 68%$244.14

A +25% CAGR over 4 years = cumulative gain of 144%

If you sumproduct every terminal probability by terminal price you get $100. And yet, while the stock is fairly valued at $100, after 4 years, you have lost money in 11/16th of scenarios (~69%). The right tail is driving the fair value of $100 while most paths take the stock lower.

This is the mathematical nature of compounding. The most likely outcomes are lower even if the stock is fairly priced.

In the real world, stocks don’t just flip up and down like coins. The probabilities are not 50/50 and there aren’t just 2 buckets they can rest in from one year to the next. The beauty of option surfaces is they allow us to separate the probabilities from the distance of the buckets (and the number of buckets is continuous…there’s no price the stock is not allowed to go to).

Here’s some homework you can do with the above data:

What’s the value of the 4-year $146.68 strike call worth?

What’s the value of the 4-year $75 strike put?

How about the 4-year $125 call?

Bonus Questions

Imagine this stock is an ETF and there’s a 2x levered version (which means it’s 2x as volatile) of it.

What strike call on the levered ETF is equivalent to the $146.48 strike on the unlevered ETF? (Hint: It’s further than $46.48 OTM)

What’s the value of the call at that strike?

If I was a market-maker and I got lifted at fair value on the 2x levered ETF 4-year 200 strike call and I go buy the regular ETF 150 4-year 150 calls to cover my risk how many do I need to buy to be perfectly hedged? (Assume you can buy them for what they’re worth…you have enough information to compute their fair value).

If you got through this then you have a new appreciation for how far certain prices are from a spot price and how it depends on time and volatility!

(Solutions & discussion in the footnotes of Well What Did You Expect)Starting from basics like the volatility tax, progressing to how path influences the volatility tax (trends are more like a volatility rebate and choppiness is a tax….the ratio of trend to chop will determine the ultimate cost of the volatility), and finally bridging these concepts to Black Scholes this series will take your understanding of compounding and how returns work to a deeper level.

Path: How Compounding Alters Return Distributions

[Between this post and the bonus questions you can start to see why pricing OTM options on levered ETFs given a liquid options market on the unlevered version is an application of these concepts]

Shout Out To Matt Hollerbach

Despite trading options for nearly 20 years at the time, it wasn’t until 2019 that I thought really hard about compounding. I knew how to manipulate formulas and how it related to options but it wasn’t until I discovered Matt’s work that I started to see it from a new angle. Matt makes it approachable and builds up insights in small steps. His blog inspired mine, especially many of my earlier posts. The entire blog is worth spending time working through. It’s similar to what I’ve said about gambling — it’s a place where you will learn how to think about risk and return far better than what finance texts will teach.

These are all-time great ones:

Solving the Equity Premium Puzzle, and Uncovering a Huge Flaw in Investment Theory

It’s painful to watch the median (or should I say average) “investor” reason about how markets work because without these intuitions (you don’t need to know formulas necessarily) you are innumerate. That’s like being illiterate but for like numbers and stuff. And the deficiency is as obvious as illiteracy is to a literate person.

The good news is we can all get better.

Stay groovy!

Substack Meetings

I was invited to be a part of the Substack Meetings beta. You can book a time to chat. I’m more expensive than a 900 number from 1988 and have a less sexy voice.

Book a meeting with Kris Abdelmessih

Moontower On The Web

📡All Moontower Meta Blog Posts

🧀MoontowerMoney

👽MoontowerQuant

🌟Affirmations and North Stars

✒️Moontower’s Favorite Posts By Others

🔖Guides To Reading I Loved

📚Book Ideas for Kids

🎙️Moontower Music

🍸Moontower Cocktails

Becoming a patron

The Moontower letter is and will always be free. My writing is a search “for the others”. The “others” are people like you who are unlearning the mental frames that artificially narrow our choices.

If you are here you already understand that inspiration is a tradable good. It’s not as tangible as a cup of coffee, but it packs 10x the adrenaline with an infinitely longer half-life than caffeine.

If you feel inspired, you can upgrade to becoming a patron.

That solving the erp puzzle link blew my mind. ERP was such a foundational part of my education that I never thought to question it, but breaking it down as individual stocks vs index seems obvious now. But please tell me vol risk premium still exists, right...