value over replacement

Moontower Munchies #97

Friends,

When Nick and I chatted late last year, he asked:

Isn’t every life decision essentially a vol trade?

I did the thing where you re-frame the question so that the answer you give gets more mileage than the direct answer. The question I decided to hear was:

“What can option theory teach us about decision-making in general”?

I transcribed my response to the question with some minor edits but afterwards, I’m going to add another point.

First the transcription:

I'm gonna piggyback off some of my training. I started at SIG, and famously—or infamously, at least in our little world—Jeff Yass has said that you cannot be a sound decision-maker without understanding option theory. That's a heavy-handed way of putting it, but what he's really pointing to is that decision-making is a practice that has structured inputs.

For example, you mentioned understanding the asymmetry or the risk-reward of a choice. An options trader would call that ‘skew.’ That’s one input into a decision—looking at the risk and reward and asking, ‘What’s the skew of this decision?’

A second component is accounting for opportunity cost. In options theory, particularly in arbitrage pricing, we think about the cost to replicate. Take futures contracts as an example: If I buy an S&P future and only need to put down a small deposit, the money I didn’t use to buy the S&P 500 outright can be earning interest elsewhere while I still have the exposure. That means the future trades at a premium to the spot price —eliminating any arbitrage. The key point is that opportunity cost is formally incorporated into options theory and valuation.

A third component of decision-making is appreciating second-order effects. I once read about something called the 'cobra effect'—I don’t know if it’s true, but the story goes that in India, there was a snake problem, so the government put a bounty on cobras. The first-order effect is obvious: more people will catch snakes. But the second-order effect? People start breeding snakes just to turn them in for the bounty, and now there are more snakes than before. In options, second-order effects are captured by Greeks.

All of these considerations—risk-reward, opportunity cost, second-order effects—are so formalized in options theory that it becomes clear how thinking in options terms can improve decision-making.

As another example:

"You and I both have a presence on the Internet—you have a YouTube channel, I have a Substack. If you think about whether to put content behind a paywall, that’s an options decision. If I paywall, I make more money today, but my reach is smaller. The second-order effect is that free content gets shared more, potentially leading to inbound opportunities that could outweigh the immediate revenue from a paywall. I write a lot, but I paywall only a tiny fraction of what I publish—essentially applying options thinking. I believe the reach is more valuable than the coupon I could clip today."

Nick: This always reminds me of Howard Marks ‘ book, The Most Important Thing which is all about second-order effects. And I think the biggest flaw in modern society, particularly in the United States, is people don't see second-order effects very well.

Me: I've often thought this in a joking kind of way regarding our politics. The right thinks everything's a slippery slope, and the left ignores second-order effects.

VOR

A concept I should have included in the interview was “value over replacement” or VOR. In options, the opportunity cost can be thought of as the risk-free rate. But the risk-free rate is an instance of a category we call benchmark.

Professional investors separate alpha from beta by benchmarking to an index. We can get fancier into benchmarking by using factors. Private investments can be subject to hurdles. All of these ideas are focused on the same question:

What is the marginal contribution of an action or intervention?

This is important because that’s what we compare the marginal cost to. We want to pay for skill not luck. Nor do we want to pay a price for skill that exceeds the amount of skill delivered.

Everyone who excels at fantasy sports understands this. In a 12-team league, the delta in points per week between Tony Gonzalez and the 12th tight end, justified drafting him in the first round. It’s not the absolute level of points anyone delivers it’s the spread from the average that matters. The “value over replacement”.

This principle is everywhere. If you are a trader who has a giant year and your discretionary bonus is nowhere near where it “should be” guess why? Value over replacement. Your firm doubts you can do it again. You’re not Tony Gonzalez, you’re a TE whose TD rate outperformed because your team got into the red zone a bit more than expected. So maybe you get paid what the replacement trader commands plus a big enough one-time premium that you are differentiated for the year but somewhere between insulted and resigned (double meaning intended). Your employer dares you to prove them wrong.*

*See adverse selection in the option job market (12 min read)

Feel like I’m picking on employees?

It applies to fund managers too. An allocator’s willingness to pay fees should depend on the dispersion of excess return in a strategy because that represents the surface area or potential for outperformance.*

If the difference between the 25th percentile and 75th percentile manager is 100 bps (think fixed income although I invented that number) then there’s not much room for fees. On the other hand, the top percent of VCs make all the money…but because the fees are roughly the same across funds,you can’t access the top ones. If they set fees by auction to where their AUM capacity clears then you’d see massive a dispersion in rakes.

(It’s like the NBA salary cap — the top x% of players are paid the same but if you had no cap, peak-Lebron would trade at multiples of other max players.)

*See Mauboussin’s Dispersion and Alpha Conversion How Dispersion Creates the Opportunity to Express Skill

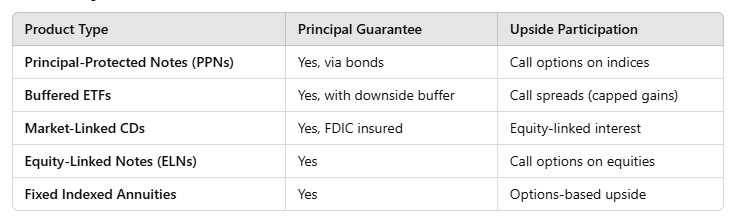

“VOR” Blindness

There’s a whole class of structures products like buffer ETFs, principa-protected notes, equity-linked notes, and fixed-index annuities that guarantee principal with a promise for upside.

They do this by spending interest proceeds on options.

The pitch sounds nice. You can either “breakeven or win”. But the pitch needs to be benchmarked to an equivalent amount of risk you’d be taking in a more vanilla form. A 90% bond/ 10% stock portfolio, bonds + calls, etc. I have major doubts that on a risk-adjusted basis, the VOR of these products after fees holds up.

They are counting on your mind’s sleight of hand in their favor — that you will benchmark performance to 0 returns instead of the opportunity cost of interest. Their AUM depends on your VOR blindness.

The Wes Anderson of Finance Podcasts

The last couple of issues I’ve linked to something from Matt Zeigler ie the cultish creative.

The reason I got on a Matt kick was the interview below. He hosts this podcast called The Intentional Investor but he asks questions about everything except finance. The premise actually didn’t sound interesting to me but I gave it a chance because my friend Jason went on the show.

So I’m 15 minutes into this and I’m like how have I not known about this Matt Zeigler dude. This is so great. Matt is just incredibly charming and endearing in his demeanor, questions and preparation (he’s known for these insane intros). Just super talented.

Now, I talk to Jason all the time. I already know he’s the most interesting man alive. But I didn’t know so much of the really early stories. Royal Tannenbaums stuff. This interview is more akin to listening to Smartless than standard investing fare. Raw, funny, and relatable. I love hearing individual’s personal stories and after listening to this you realize just how under-done that it is. I’ve never heard such an in-depth life story in an interview like this that wasn’t just background to what the person is doing now. What you were doing when you were middle school is as much the point as anything else happening in this discussion.

If you’re into podcasts I think you’ll agree that this is super fresh format. Matt also strikes me as the perfect host to pull it off. I went in with low expectations and it was awesome, unfortunately after writing all this I can’t send you in the same I went in but I get stoked when dig things so there ya are.

Quant Bootcamp

Ricki Heicklen’s Quant Trader Bootcamp is coming back to the Bay Area Feb 12-17th.

I spent a day at her last session and was totally blown away. Gigabrain ex-Jane Street traders giving a heavy dose of what trading logic, argument, reasoning, and quant heuristics in a 100% hands-on way.

Check out the testimonials page to hear what others thought.

On Nov 10th I wrote:

On Thursday I attended and had a chance to talk to Ricki Heicklen’s Quant Bootcamp. There's just nothing like this. It's ridiculous. Unless you get an internship at Jane St, this is the closest glimpse you are going to get to how they (and a few similar firms) think.

If you get a chance, do it.

Now you have a chance. Use the promo code MOONTOWER at checkout to get $150 off. I’ll be swinging by the BootCamp to give a chat again and even better learn more stuff!

Stay Groovy

☮️

Need help analyzing a business, investment or career decision?

Book a call with me.

It's $500 for 60 minutes. Let's work through your problem together. If you're not satisfied, you get a refund.

Let me know what you want to discuss and I’ll give you a straight answer on whether I can be helpful before we chat.

I started doing these in early 2022 by accident via inbound inquiries from readers. So I hung out a shingle through the Substack Meetings beta. You can see how I’ve helped others:

Moontower On The Web

📡All Moontower Meta Blog Posts

👤About Me

Specific Moontower Projects

🧀MoontowerMoney

👽MoontowerQuant

🌟Affirmations and North Stars

🧠Moontower Brain-Plug In

Curations

✒️Moontower’s Favorite Posts By Others

🔖Guides To Reading I Enjoyed

🛋️Investment Blogs I Read

📚Book Ideas for Kids

Fun

🎙️Moontower Music

🍸Moontower Cocktails

🎲Moontower Boardgaming

Chris Cole has a paper about Wins Above Replacement – the basic gist of it is if you were to lever your portfolio so you keep 100% of your prior exposures but add an overlay, would your portfolio be better off overall with what you are adding? He then turned that into a metric.

You may have already read that paper, but in case you didn't (or in case other readers haven't), now you know it exists.