Moontower #128

It Might Be Passive, But It Ain't Income

Happy Thanksgiving weekend!

This week’s Money Angle will be interesting to anyone who fits any of these categories:

Has a financial advisor

Reads books with the words “passive income” or “financial freedom”

Knows what an option is

Money Angle

First something nice. An amuse-bouche:

That was pleasant enough.

Now violence.

You have heard of selling calls for “passive income”. The pitches which promote this idea are using the word “income” in the same sense that I would earn “income” if I sold you my house for $100. The income is a receipt or a cashflow, but this is just mechanical accounting. I have not earned income in any economic sense of the word. A receipt is not income without considering value given vs value received.

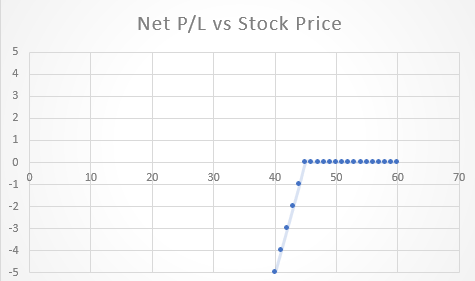

Suppose you own a $50 stock. Imagine you sold the $45 strike call for $5. Imagine the scenarios:

Stock goes up: Let’s say it goes to $60

$10 profit on stock holdings

Call option you are short goes up by $10

You are assigned on your call option, your stock is called away, leaving you with no position. P/L =0

Stock falls but remains above the strike: Let’s say it goes to $47

$3 loss on stock holdings

Call option you shorted falls to $2. You earn $3 on that leg.

Again, you are assigned on your call option, your stock is called away, leaving you with no position. P/L =0

Stock falls below the strike: Let’s say it goes to $40

$10 loss on stock holdings

Call option you shorted expires worthless. You earn $5 on that leg.

Since the call is worthless, you still own the stock and you have a net loss of $5

A few things to observe:

You can only lose. This makes sense. You sold an option at its intrinsic value. Visually:

These scenarios are exactly the same as if you held no stock position and you sold the 45 strike put at $0. This is called “put/call parity”.

Parity means equal. It means a call is a put and a put is a call. Your stock position combined with the option you are long or short determines your effective position.Long stock, short call = short put (this is all covered calls!)

Short stock, long call = long put

Long stock, long put = long call

Short stock, short put = short call

You can prove this to yourself by making up more scenarios as I did above. Draw those hockey stick diagrams to summarize.

So when you sell a call against your stock position, you are now saying “I prefer total downside and limited upside”.

Is the call worth selling?

Nobody says “I prefer total downside and limited upside”. But bond investors choose this all the time. Because the relevant question is about PRICE. Any proposition can be ruined or alluring depending on the price. An option’s price is simply a future state of the world discounted by its probability.

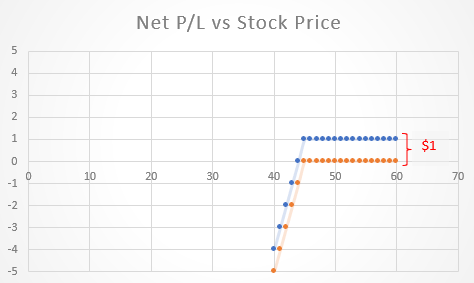

When you sell an option, you don’t earn income. You just bet against some future state of the world. Whether this was a good idea or not depends on the price. Price is the market-implied odds. The actual odds are an imaginary idea. Price is a flesh-and-blood painting of the idea that you can interact with. Unless your day job is to figure out if the depiction of that idea, the price, is accurate, it’s best to assume it is.Suppose, instead of selling that 45 strike call for $5 you could sell it for $6. This parallel shifts the hockey stick $1.00 higher.

This is a more attractive pay-off, but as a covered call writer, you need to ask yourself…is it attractive enough? Let me answer for you.

You have no idea.

What would you need to know to even evaluate the question “is it attractive enough”?

You’d need to know something about the odds of the stock making an X% move by the expiration date. This is mostly what we mean when we say “volatility”. How will you know those odds? You can’t. You can only guess. And that’s what the price was in the first place. The wisdom-of-crowds guess. Do you have a reason to believe you can beat the line? What do see that option price-setters don’t?

Professional volatility traders have an opinion as to what the fair value of the option is. If they sell an option for more than its alleged “fair value”, some internal accounting systems may allow them to book the excess premium as “income”. But they would call that “theoretical edge” or “theo”, not income. And even that edge is taken with truckloads of salt.1

How To Respond To Your Advisor

If [insert “options as income” advisor] thinks you should sell calls ask them:

Is the option overpriced?

They won’t say no. They probably also won’t say yes, since how the hell do they know. They’ll say:

“You’ll be happy if the stock gets there.”

Sure you might be happy if the stock goes to your strike. But that’s cherry-picking the point of maximum happiness for any short option position. It’s literally, the short option position’s homerun scenario. Your broker is selling you on the best-case scenario. The remaining win vs lose scenarios are painfully asymmetric:

In a scenario where the stock goes up a lot, you are getting unboundedly sadder.

In the case where the stock goes down a lot (assuming you weren’t going to sell no matter what), you are better off by the amount of the premium you sold, which is capped.

Do not benchmark your opinion of the trade to stock-grind-up-to-my-short-strike scenario.

The Main Takeaways

In the single stock game, you cannot afford to NOT get piggish results on the upside since most single stocks have awful long-term returns. You will be sad if you invest in securities with unlimited upside but systematically truncate that upside.

Here’s a link to the document I wish I wrote. It’s highly intuitive. It does better than explain. It shows how you are incinerating money if you are selling calls below what they are worth even when you are “just overwriting”.

Final Word

It’s possible your advisor doesn’t totally grok the concept as laid out in QVR’s document or even what I wrote about. They have been bombarded with so much callsplainin’ that the discourse has been vocally one-sided. This post is probably in vain, but perhaps one RIA at a time, we can move past “selling options for income” as they internalize that:

The price of the option is central to the proposition.

Since what drives price is complex, any discussion about the attractiveness of overwriting becomes more nuanced.

As far as option promoters and authors who treat an entire premium as passive income? Clowns.

If I’m aggressive in saying that it’s because the overwriting fetish is so widespread, there’s nothing to do but make people feel bad about a naive, unsound practice that hinges on “you’ll be happy anyway, even if you lose”. That’s utter garbage. The difference between a winning poker player and a losing poker player might be a single big blind per hour. You cannot afford to just piss away expectancy.

So when you see these promoters you can safely dismiss them as charlatans. We need less of those these days.

You’re welcome for the very simple, reductionist negative screen. I just saved you many hours of brain damage, a trip to Orlando for that “Make $10k Per Week” options seminar, and the $899 “course materials” emblazoned with a pic of someone who probably looks like me2 with slicked-back hair in a rented Lambo. You can smell the Drakkar Noir from the glossy page.

Actual option traders don’t wear suits. And they don’t tell you to sell calls for income.

It’s possible that a price has a bunch of donkeys on one side and sharps on the other. Donkeys might be dumb but they have numbers. They can push prices to a fat enough risk premia that the other side is all sharps, as opposed to a balanced Jane-Street-bid-offered-at-CitSec line (or what I’d call a round or fair market as opposed to one that is leaned like a jewelry store at a Caribbean cruise stop. The introspective reader is now wondering “how do I know if the market is leaned?”)

So if you argue that the price is obviously wrong, you need to explain how you were able to spot the donkey line. Even then, a donkey line often becomes one because the flow has overwhelmed the limits of arbitrage. It is unmoored to reality or, even better, driving the reality. The edge in selling it embeds path risk, gap risk, liquidity risk, mark-to-market risk. It’s a pile of risk that is nearly impossible to hedge beyond simply not trading too big.

In the words of Alanis Morrisette…ironic.

I agree that covered call option writing should not be described as producing income. Should one use the term income for the higher yields of corporate bonds, especially junk bonds, compared to Treasury bonds? The higher yields are produced by effectively selling puts or taking liquidity risk.