loving the alien

Moontower #245

Friends,

If you know about education and want to write about it, I’m just letting you know you should go for it. There’s an audience. That Principles of Learning jam I put out Wednesday got me a lot of inbound. Which I never would have predicted. It was an exercise in organizing my thoughts on a topic I find inexhaustibly interesting — learning faster and more efficiently. If I wasn’t loving building moontower.ai, I’d be pulling on that thread harder.

[If you are operating at the intersection of machine learning and human learning and want to connect hit me up. I have a close friend at the tip of that spear who I’d be asking for a job if I wasn’t being feral.]

Anyway, parents wanna know about this stuff based on my email inbound. Just sayin.

In that vein, I’m going to share a response I sent to someone who recently enrolled their 7th grader in Math Academy. The parent is concerned that by going faster (even in a selective private school that the child is already in) that boredom could become an issue.

I’ll be honest. I hadn’t considered that angle. But it’s a totally legitimate one considering that MA’s Justin Skycak addresses it directly in:

The Greatest Educational Life Hack: Learning Math Ahead of Time (5 min read)

Justin frames it in terms of risk and reward. That’s a valid approach. But for some kids, it’s still too conservative. Pre-learning is the ultimate option on having doors open that simply won’t any other way because you are compressing time.

In one of Paul Graham’s best essays, How To Make Wealth, he talks about the decision to join a startup in such terms. In Startup = Growth it’s spelled out — “raising money lets you choose your growth rate”. If the kid enjoys going faster, let ‘er rip, they aren’t aware of the option your giving them but they might thank you later.

[I wish I could make copies of myself to do all the stuff I want to do but at the same time, I consciously don’t want to burn the candle at both ends right now. There are doors that are closed because I didn’t go faster when the cost of going faster from a family POV was lower. But I wasn’t inspired to go faster then. Anyway, I’m not writing for therapy here, but if I’m projecting my own illusions you should at least have the disclaimer. ]

I suspect the downside is not especially sensitive to pre-learning anyway. Even if a motivated or math-inclined kid didn’t pre-learn they’re gonna be bored. The teacher will introduce a topic, the kid will get it immediately and still need to wait for others to catch up.

Something I tell my kids, and I don't express it any type of subversive tone but just as a matter of fact...you can't let the pace of school dictate what you think is a normal pace. School is built for everyone, but if you are good at sports you wouldn't expect to move at the pace of the average kid in your class. You'd have a coach and play “up” or on a club team.

The subconscious message we pick up everywhere, especially in school, is that there's a correct pace. But the error bars around that pace are massive. We know our children so deferring to what's best for the average when we have specific info (whether they need more help or more stimulation) is wasting info. As always, it’s sound decision-making hygiene to consider the outside view but adjust it for your circumstances.

One last caveat — if I found out my bored kid was working on his fantasy football model underneath this textbook at school because he was bored my reflex would be “Sweet, show me what you got so far. But also you better get an A+.”

Money Angle

In a moment of procrastination I went to Twitter and found something to spout off on.

It’s about the coverage of the election.

Ha, ha, yea right. I’d rather piss razors than talk about politics, thank you very much.

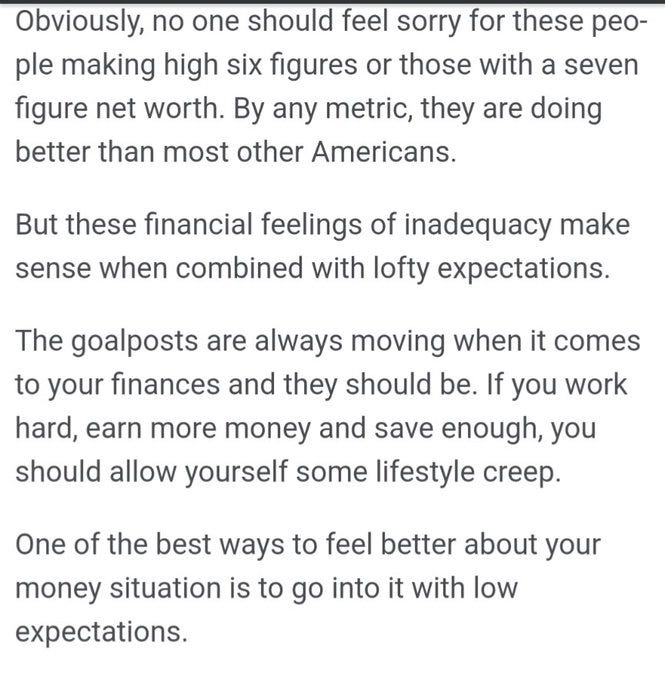

I did peek at Twitter and though I’ve seen some story about people making 6-figures feeling broke for the millionth time, I failed to contain my need to pop off this time. Actually, the triggering source material is totally innocent. It’s a nice post by Ben Carlson, one of the first finance bloggers I started reading about a decade ago when I first started trying to learn about investing (I’m a trader and trading is not investing).

I tweeted his excerpt with my thoughts. I reprinted a lightly edited version below the screenshot. It’s in reference to HENRYs (high-earner-not-yet-rich), an acronym nobody in the history of the world has ever uttered without a derisive smirk. In some circles, they are known as the “working rich”.

I’m sorry but if you’re actually rich you don’t think of these people as rich and if you’re a regular person you don’t consider these people working class. This acronym is the personal finance version of the “finger cuffs” nickname memorialized in Chasing Amy. You’re under 50, live near the coast, and are worth $5-$15mm. Congratulations, the inflation you moan about also went into your income.

Let’s just get to the sauce already.

The tweet thread:

This post is fine, reasonable posture. ...but if I may piggyback off some of the numbers in the post... I want to repeat what the post says but with slightly different emphasis which leads to a large difference in framing.

For example, it talks about people in the top 5% of income or wealth being disappointed, and you'd be better off going in with lower expectations.

When I think the harsh but true reality is being in the top 5% when you measure against the whole population just... isn't that special.

When I was a kid, being rich was like Robin Leach stuff. It felt totally unattainable. And you know what? It is. Rich, as defined by its day, is unattainable.

Of course, someone will say, "Actually, it is attainable," and my argument is... it's not for people who complain that they don't feel rich or whatever. Because the mindset that comes with Robin Leach-level desire would never accept the top 5% as being entitled to anything. It's a failure.

So when the article says to lower your expectations, my reframing is: get serious about what being excellent means. You're not even close if you're a top 5%er. So either get serious about what it takes to be rich, or be seriously gracious for what you've gotten. All the woes of inflation and yadda yadda hit everyone.

You're still stack-ranked in the same relative sense. Moaning is so unbecoming; it feels like such a confession of how duped you were by thinking school was real life or that X dollars mapped to Y.

I just don't feel like being rich is something I should ever expect unless I'm so badass that I'd be comfortable being at a table with people that are unmistakably badass.

You're a PM at a tech company and you don't feel rich? Of course you don't. You shouldn't. You're not scarce AF. You haven't taken a massive risk and come out on the other side.

The fact that there are normal people who became very rich by being in the right place at the right time shouldn't influence your expectation of that likelihood.

(Houses are so expensive where I am not because everyone is a celeb... it's because I live within 50 miles of "I've been at Google/Pinterest/CRM/Dash since pre-IPO." That's called hitting the lotto. Most of the people in tech who have been around for 20 years have been bouncing around from one high-paying job to the next but falling short of the exponential. I use this analogy a lot.)

To get where I got in my career required flipping heads 10x in a row and tremendous effort. That earned me comfort. But to become one of the bosses who are ballplayer-rich, I'm probably staring down another chain of 10 in a row. I don't get that life in this life. I'm lucky to be anywhere near the one I got, but it's utterly unremarkable, and this is inclusive of being very good at my job.

Smart, hardworking, etc. Table stakes. You're not special. Comparing your 5%-ness with the masses is nothing more than a poorly adaptive exercise in self-flattering benchmarking.

I suspect the mambas are looking to transcend comparison and would never use it to self-soothe or justify. If you want to feel rich, expect alien powers from yourself instead of expecting that being way above average should entitle you to an alien life.

No looking over the fence at others.

Look in the mirror. Are you doing truly alien shit?

That’s that.

It’s an excuse to insert some Velvet Revolver.

Money Angle For Masochists

Portfolio Vol 101

I trimmed the video from Thursday down to a 15 minute section that gives an education as well as a step by step implementation of computing portfolio vol. There’s even a little detour into dispersion.

On my aversion to trading implied skew

First of all, free subs to moontower.ai can access a few tools and reading materials as well as the community but they cannot post and can’t see analytics.

Here’s a question that was posted in the community this week:

I was reading thru an old tweet of yours on trading skew. The tl;dr of the tweet was don't trade skew... Given I am in a masochistic mood, how would one go about backtesting a skew trading strategy?

I had 2 ideas, which I'd love to get your thoughts on.

Idea 1:

X asset 25d 3M normalized put skew is in the 100th percentile, sell a 25d put strike, delta hedged

hedge the delta daily or at some discrete interval

check how this strat would have performed assuming the trade is held until expiry

Idea 2:

X asset 25d 3M normalized put skew is in the 100th percentile, sell a 25d put strike, delta hedged

wait until normalized skew returns to some threshold, for example 75th percentile

hedge the delta daily but close out the trade as soon as the threshold is hit

Lots of questions, but the main ones are:

for idea 1, does your pnl depend on implied skew vs realized skew (similar to implied vol vs realized vol). How would you measure this?

for idea 2, does your pnl depend on a combo of realized skew (for as long as the trade is held) as well as surface repricing (ie selling at 100th percentile implied skew and closing out at 75th percentile). The thought of measuring this gives true masochists vibes, but how would you?

I wonder if the juice is worth the squeeze? Meaning, assuming you built the foundation to measure/test all the above, is there really any pnl in it / are you better off focusing on VRP trades?

My response:

As a matter of practicality, I think the test should be more in the vein of idea #1.

If you consider skew percentiles, the difference between the the 25th and 75th percentile could be some absolutely small number like 2 vega points. And the level of skew itself measured by percentile is sensitive to the percentile lookback such that the range you are trading over is just quite small. Your interim p/l will be the sum of implied vol change but plus realized delta hedging p/l.

But consider this...let's say you sell the 25d put and it becomes a 50d put but the skew normalizes. That skew metric is no longer referencing your position. You have a floating vs fixed problem. In other words, you can't really trade implied skew directly.

Your results are basically going to come down to path. Your interim p/l is going to get marked based on the IV of the fixed strike you have on and that in turn is going to influence the delta you hedged on.

The delta you hedge on is going to have a large impact on your final p/l so it's not just where does the stock go but what deltas were imputed along the way. For example suppose you run a model with spot/vol correlation embedded in the SP500...this will generate higher OTM put deltas.

If the market trends down you will win to this but vice versa. However, if you used B-S deltas you will get hurt as the market goes down and vice versa. And even then, you will def get hurt on the marks, but if the stock expires near the short strike you will probably still win by expiration even though the mark-to-market path is hairy.

I used to work with a big oil options trader that would on a monthly basis stick a hedged 1-month risk reversal in a separate account and hedge it on B-S deltas. My point is that is an active choice that influences the results. Another choice could be to hedge on deltas that don't incorporate implied skew at all but just use ATM vols.

Overall, testing the idea, even a monte carlo, is a great way to get a shape of the problem but more importantly because you can see how the parameters you choose impact the p/l path.

I'm not kidding when I say skew trading is masochism. If oil is $75 and has massive put skew and the market drifts down to $55 and the skew gets hammered (so say the 40 puts don't perform) but you sold the 60 put what skew did is irrelevant. All that will matter is how fast did the stock go to $55 and what deltas were you running on the $60 strike along the way.

The weirder the distribution the crazier this is. I've seen nat gas option traders blow out being long put skew on a 15% drop in the underlying because they used too high of an implied option delta and they delta hedged several times on the way down.

Had they they run a lower vol and delta OR hedged less they might have survived. There's not much lesson from this other than...sometimes a 15% selloff is interpreted by the market as "stabilizing" and sometimes it's destabilizing and that is what's gonna dictate the options behavior.

From My Actual Life

This week I found the thing my 8-year-old thinks is the funniest thing in the world.

Live action Butthead.

I’ve had never seen this skit before but Max and I were down a rabbit hole of SNL cast members breaking character after we watched a few segments from Nate Bargatze last week.

There is a great moment in the skit above a character breakage. We’ve watched it 15 times this week at least.

The rest of our week was kept light by the fact that Max is now walking around the house imitating Bill Hader doing impressions of Arnold Schwarzenegger.

You don’t wanna miss this one:

Max is also loving Fred Armisen, Kristen Wiig, and especially The Californians skits which are god-tier imo. I gotta catch Max on video doing Arnold…"Cahm ahn, show mee your leedahship cape-ah-beeleeties!"

Stay Groovy

☮️

Moontower Weekly Recap

Need help analyzing a business, investment or career decision?

Book a call with me.

It's $500 for 60 minutes. Let's work through your problem together. If you're not satisfied, you get a refund.

Let me know what you want to discuss and I’ll give you a straight answer on whether I can be helpful before we chat.

I started doing these in early 2022 by accident via inbound inquiries from readers. So I hung out a shingle through the Substack Meetings beta. You can see how I’ve helped others:

Moontower On The Web

📡All Moontower Meta Blog Posts

👤About Me

Specific Moontower Projects

🧀MoontowerMoney

👽MoontowerQuant

🌟Affirmations and North Stars

🧠Moontower Brain-Plug In

Curations

✒️Moontower’s Favorite Posts By Others

🔖Guides To Reading I Enjoyed

🛋️Investment Blogs I Read

📚Book Ideas for Kids

Fun

🎙️Moontower Music

🍸Moontower Cocktails

🎲Moontower Boardgaming

Hey kris I remember your interview question to construct a positive vol convexity trade. Can you sometime later in future posts address the mechanism and optimal time to put such structure on.

Thank you!