Foreplay For Option Enjoyers

Moontower Munchies #47

Friends,

The cat is not quite out of the bag…

…but it will be soon. More to say on this on Sunday.

For now, a new post.

👁️A Visual Appreciation For Black-Scholes Delta (Moontower)

It’s better to read it thru the link because the colored fonts will make it easier to understand the equations. If you insist on reading it here:

I was messing with the Black-Scholes equation and happened on another way to visually understand it.

A prerequisite for appreciating this angle is to be familiar with Black-Scholes in the first place. If you aren’t and would like an intuitive understanding of the equation check out: The Intuition Behind The Black Scholes Equation.

This is a review of what you need from that post but if it’s still foggy you can go back to the whole post.

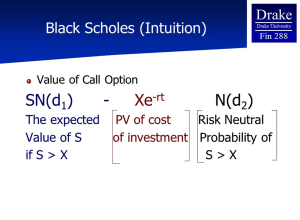

This is the B-S equation:

The equation was born from a principle of no arbitrage:

If you can replicate the cash flow of an asset with a strategy then the price of the asset should equal the cost of executing the strategy.

The left-side of the equation (ie the call option price) is the asset

The right-side of the equation is the strategy

Construct a long/short portfolio:

Short the call (the left-side)

Long the strategy (the right-side)

Strategy – call = 0 profit

The call price must equal the p/l of the strategy for there to be no arbitrage.

The right-side of the equation is the strategy that replicates a long call option. (To offset the actual call we are short)

Let’s break this down step-by-step:

That strategy is a portfolio

The value of that portfolio at expiration discounted to present value must equal the value of the call option today

The portfolio has 2 components:

Shares: We need long shares of the underlying stock

Cash: We will need a loan to finance those shares (An important idea in derivates pricing via arbitrage pricing is that we assume the strategy is “self-financing”. That means you don’t need money to start. If you respond with “But I do have some money to start”, the self-financing paradigm is already taking care of the opportunity cost using the RFR. The computation remains valid.)

How much cash and shares do we need?

1) Share quantity in the portfolio

The amount of stock you need in this replicating portfolio is weighted by the expected value of the strike being in the money. Notice we say “expected value” which is not just probability but probability x payoff. The phrase expected value of the shares going in the money is what determines the delta or hedge ratio of the option.

Delta = N(d1)

Share quantity = S*N(d1)

2) Cash quantity in the portfolio

We need cash to finance the purchase of those shares. If we are short the call and it goes in the money we know we will receive the strike price at expiration because the long option holder will exercise the call and we will sell shares to them. If the shares were 100% to be in-the-money then we know we would receive the strike price at expiration. For example, if you sold a call option struck at $125 and it was 100% to be in-the-money, you are certain to sell the stock at $125 and receive that much cash at that future date.

Of course, the option is not 100% to be in the money. So we discount the strike in 2 ways:

By the probability that it will be in the money

By the risk-free rate, to get it in present value terms

We can now say, on average, you will receive the present value of the strike weighted by its probability of being in the money.

Probability of strike being in-the-money = N(d2)

Again, this is just expected value logic. We weight the present value of the strike by its probability of being in the money.

Cash quantity = PV(strike) * N(d2)

This ends the review. The next section is new material. If this is still foggy zoom in on this part of the B-S primer: Animating The Equation

Visually Representing These Quantities On The Distribution

First, let’s ignore interest.

Remember:

N(d1) = delta

N(d2) = Probability stock (S) finishes > strike price (X)

Call = S * delta – X * P(ITM)

Here’s the logic to go with the picture:

You are replicating a long call option with a mix of shares and cash.

1. You will need to sell a zero-coupon bond at X * P(ITM) to buy the stock

Why that amount?

This is the expectancy or probability weighted cost of buying the stock at the strike. Remember, no-arbitrage replication pricing must be “self-financing”. We need the proceeds of the expected cost of the shares today so that becomes the face value of the zero-coupon bond we sell.

2. We will spend the proceeds of the zero-coupon bond to buy shares today. How many shares do we need to buy?

We must buy S * delta shares. So if the shares are $100 and the delta of the option is 30%, we need to buy $30 worth of stock.

However, there’s a problem.

We can’t afford that many shares with our current proceeds!

Why?

Because this is true:

X * P(ITM) < S * delta

Why is this true?

Because S * delta is the expectancy of the stock given it expires higher than the strike X. It’s the sumproduct of all stock prices above X weighted by their probabilities (ie integral of the PDF).

That quantity must be larger than X * P(ITM) which is the probability of the stock being above the strike times the [single point] strike X.

[Note: This idea is also captured in the fact that d1 > d2]

This shortfall in shares we can afford to buy with the proceeds of the zero-coupon bond sale is what the call option must be worth!

This is the essence of B-S. The call value is balancing price that equates the option to the cost of the replicating portfolio.

A Visual Decomposition Of Delta

We got this:

Call = S * delta – X * P(ITM)

Let’s re-arrange this equation to be in terms of delta.

delta = [ Call + X * P(ITM) ] / S

in words:

delta = (Call + weighted strike) / S

We know delta is a hedge ratio between 0 and 1.

Observe:

The lower the weighted strike the more the delta looks like call price/stock price which will be small value

If the weighted strike is high because P(ITM) is high, then the call/stock will be closer to 1

We can simplify this even more by noticing that dividing by S is just normalizing by the stock price. In fact, if the stock price is $100 then this will be true:

delta x 100= Call + weighted strike

The 100 just gets in the way of the intuition and is safe to ignore for our purpose. It’s just a scalar. We can see that delta can be simply decomposed as:

delta = Call + weighted strike

This decomposition is more satisfying visually. But before the grand reveal let’s just be thorough and validate that this calculation of delta matches what my B-S calculator says (it does).

Let’s also remember what the chart of call delta by strike looks like:

Putting it all together:

Notice:

When the call is deep ITM the delta is driven by the expensive call value which is made of lots of intrinsic value. The proceeds of the zero-coupon bond represented by the weighted strike price is extremely low, so the call must be expensive.

As the strike becomes ATM and eventually OTM the value of the call gets cheaper. You are able to buy more shares with the proceeds of the weighted strike, so the call is doesn’t need to be worth as much to balance the cost of the replicating portfolio.

As interest rise, the discounted strike (the amount you can collect from selling a zero-coupon bond) declines, meaning you can buy less shares to replicate the option. So the call option must be worth more. This is why call options have a positive rho or sensitivity to interest rates.

It’s neat to think of delta as the ratio of a call price + the weighted strike to the stock price. If you consider the price for an OTM call, you realize its delta is entirely driven by the ratio weighted strike / stock price

And for some completeness, this is a simple chart decomposing the call value into delta hedge – weighted strike (again assuming interest rates are zero)

Overall, this post is grout in your options thinking. It helps make connections between various concepts by showing you them from a different angle.

☮️

Stay groovy

Need help analyzing a business, investment or career decision?

Book a call with me.

It's $500 for 60 minutes. Let's work through your problem together. If you're not satisfied, you get a refund.

Let me know what you want to discuss and I’ll give you a straight answer on whether I can be helpful before we chat.

I started doing these in early 2022 by accident via inbound inquiries from readers. So I hung out a shingle through the Substack Meetings beta. You can see how I’ve helped others:

Moontower On The Web

📡All Moontower Meta Blog Posts

🌕Welcome Traveler

This " .AI "not only looks promising; but the best ever data mining for tool for retailers I've ever seen.

Congratulations for your work. Let sunday soon be there .....