🌙Last Call🌙

The moontower.ai holiday sale continues.

Click here to sign up and use BLACKFRIDAY at the Stripe Checkout page to get 30% off any Moontower subscription including our new Starter Plan.

Friends,

The recent Economist lead article:

Meanwhile in reality:

I know it’s quaint in 2024 AD to let reality get in the way of a good story but this is what we know:

The online sports betting industry is a low-margin business with high customer acquisition costs (ie relentless advertising and bonus promos).

Like mobile gaming, most of the profits come from a small subset of customers. You can dress this up in VC-approved language: 80/20 rule, Pareto distribution, power law. But in gaming, these high-value customers are simply called “whales”. In sports betting, the right word is “addicts”.

The profits come from sick people who churn. And why must they churn? Because eventually, they go broke betting 4-leg parlays. What’s a 4-leg parlay? It’s a clinical term for when a gambling site connects a Dyson to your bank account.

If your best customers necessarily churn you have no choice except to hunt for more sick people and make sure you exact every last cent out of the ones you’ve hooked.

The entire regulatory backdrop is complicit in a gigantic lie — that this is a free market. But you’re not allowed to win. It’s a rigged game. If you have an edge they limit your bet sizes to lollipop levels.

The gambling 800 number PSA they include in the ads is weapons-grade irony. The business relies on the people who should be calling that number to instead believe that their luck is about to change for the better.

Any attempt to rebut the disgusting contradictions with rhetoric (nobody is going to defend their behavior honestly with data) must contend with reality — sharp bettors try to mimic addicts or blend in with edgeless whales to “get down” (lingo for being able to place adequate sized bets). That tells you everything about the industry’s sympathies towards addicts.

Anyway, I had no reason to bring any of this up except for the Economist cover being a cat’s paw for hyper liberal market ideology. There are plenty of examples of free trade being pro-sum. This one undermines the message. An impressive journalistic own-goal for a publication titled “Economist”.

Make me czar and I kill the current system. Instead…all betting is on an exchange. You bid and offer just like futures markets. It won't solve addiction but now smart bettors are valuable and rewarded, everyone gets better prices, and the incentives are towards volumes not seeking out sick people to cross faded markets.

More reading:

The Online Sports Gambling Experiment Has Failed (14 min read)

Zvi Mowshowitz

While I’m just ranting, Zvi shows his work in a convincing argument.

[Zvi is a sports gambler and a former Jane Street trader. His discussion of trading in this interview with Patrick McKenzie is fun.

Zvi’s substack tends to be mostly focused on AI but he does deep dives on various topics. The recent one on the Jones Act is shockingly hard to put down. The subject would appear to be dry (no glancing pun intended with Jones being about water-borne trade) but Zvi brings it to life.]

Related:

✍🏽Takeaways from The Odd Lots episode with pro sports gambler Isaac Rose-Berman

✍🏽Classics that remind us that thinking in averages or bell curves is often dead wrong. In many domains, especially business, a small number of customers or products drive most of the outcome.

Taylor Pearson’s How to Get Lucky: Focus On The Fat Tails (13 min read)

Kevin Kelly’s 1000 True Fans (19 min read)

I didn’t read Kevin’s post in 2008 when it dropped but it turned out to be incredibly wise.

On a related note, I owe you a thank you. Crossed 15k this week. The letter resumed strong growth, similar to early 2022, before the Twitter algo devalued my use of it by suppressing outside links, esp substack. Growth this year was brute force — I never wrote so much as in 2024.

Most importantly thank you for the privilege of not letting me talk to myself any longer than I already do.

Money Angle

A couple things upcoming this week.

Kris Longmore at Robot Wealth whose incredibly enlightening and generous story I boosted in case study on becoming a partner at a trading firm is hosting me for a live AMA with his community this Wednesday.

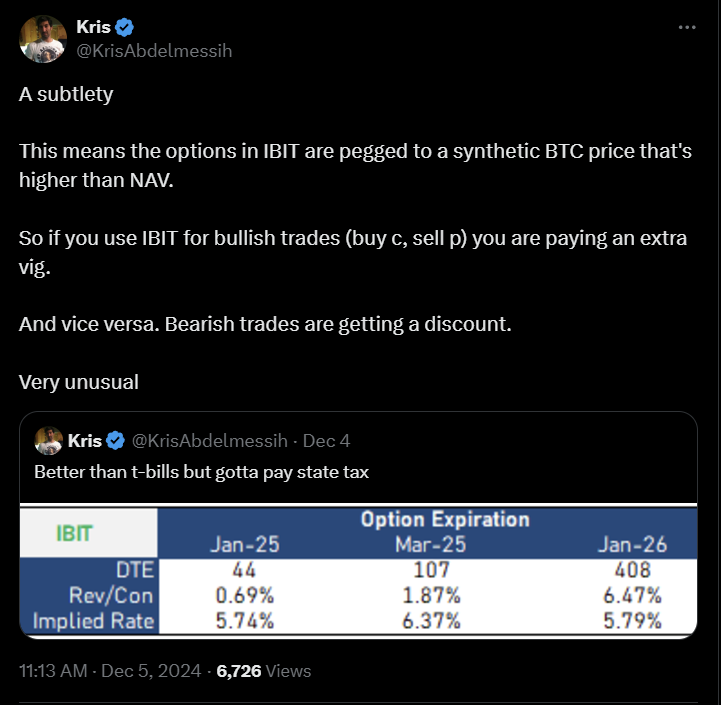

If anyone asks me about BTC I’ll discuss my frustration with this dynamic in the option market (that’s a tell by the way):

In English, the tweet shows how IBIT is trading richer via the options than the cash price of IBIT shares. That means if you buy the IBIT synthetic future via the options you'll underperform just buying IBIT. Likewise if you short the synthetic you will outperform an IBIT short.

Money Angle For Masochists

On Thursday I published a post called laying in the weeds, an expression I used regularly. Whether it was getting ready to pounce on an offer that accumulates suddenly, sniping with electronic eyes while streaming, or just keeping your mouth shut while others leak info, the lingo fits. It’s ultimately about execution — how do I get the price and size I want?

We can use that background to riff about execution which is easy but dangerous to develop lazy habits about (like laying in the weeds this is more of a professional topic because of the imperative to reduce slippage)

Here’s a common scenario in the voice option market.

Assumptions:

An option is worth $.90

A broker is bidding $.92 for 10,000 lots

You and 3 additional market makers are offering at $.94. You know this because the broker, who we will assume is honest, relayed the full picture.

The case of simple 2 choice scenario tree

You hit the bid and get all 10,000. Expected profit = $.02 x 100 x 10,000 = $20,000

Nobody breaks rank, the offer is lifted with 4 market makers getting equal allocation. Expected profit = $.04 x 100 x 2,500 = $10,000

Seems like you should hit the bid. Except for that, if you do, next time all the offers are more aggressive. Tit-for-tat mutually assured destruction.

You get an interesting result if you unravel the game theory. Assuming none of the market makers are particularly axed in the option, and they all have a similar hurdle rate on how much capital they are willing to deploy for some amount of risk/reward you end up with a stable equilibrium that looks similar to what pre-communicated collusion would have resulted in.

[Aside from the dinosaur era: The way to get a lightly capitalized newcomer to your options pit to give up and go home is demoralizing attrition — trade everything for fair until they go away. I even remember days as a clerk on the specialist post where the boss would tell me to offer something so cheap on our exchange to embarrass a specialist on another exchange who ripped off the buyer at a higher price. The away specialist could lift our lower offer and lock-in a profit but they wouldn’t want to because by forcing the print they would make the customer feel bad about their fill. And if they did lock in the profit by trading with us, we were more than happy to incinerate money to make the customer think twice about routing around us in the future. I can remember the boss, crossed arms, still as Vader: “Keep offering. Filled? Reload.”]

More than 2 choices

Realistically, there are many scenarios. The option could have traded $.92 or $.93 with similar splits even if the first trader who hits the bid thinks she is getting the full bid size, but the broker being a diplomat who needs to deal with each of the market-makers daily decides to split it 4 ways anyway at the lower price. This result is common and explains why it doesn’t make sense to break price. They are unlikely to get the benefit unless they clarify with the broker that they are only going to hit the bid if they get full size (the broker weighs whether they should box the other 3 out and consequently piss them off).

How this plays out depends on your business relationship to the broker both in terms of how much you pay them and how useful you are in making fast, tight markets. When I was a local on the NYMEX I didn’t trade huge size but I was super-responsive so I could get those 25 and 50 lot berries. Those tight markets were also useful to the brokers who could use them “cuff” a related market or fish for business. At the fund, my value in the ecosystem was size, so I had leverage in setting the price of a larger order (maybe I could convince the broker to make the splits 4k, 4k, 1k, and 1k where I’m one of the larger allocations) but didn’t get the small layup orders.

We can get bogged down in scenarios forever, but the point is that this little game is being played all day. In the voice market and the electronic algo logic of sophisticated market-makers. If I divide all my profits by how many contracts I traded I end up somewhere in the penny ballpark. That’s the margin. That’s the difference between tossing coins for fair and a highly profitable business. It also means, that without a lot of reps it’s hard to tell if you have an edge.

Let’s do another example of cat-and-mouse.

An option is quoted $.21-$.23

You think it’s worth $.25

What do you do?

The correct answer is “it depends”. The first step to building a model for solving this execution problem is to identify the dependencies.

A few off the top of my head:

If I lift, I make $.02 of edge on Y volume

If I join the $.21 bid, what’s the probability I get hit (therefore making $.04) and how much volume would I get? Handicapping this depends on if the matching engine is time priority or pro-rata as well as if there is any priority that derives from my designation (customer, pro customer, professional, and more)

If I bid $.22 and get hit I make $.03. But would that bid cause someone else to lift $.23s? I need some map of what other market observers think an option is worth.

Broadly, I need some priors about the distribution of what others think this option is worth based on existing bids/offers, the trades that have happened, and trades that have not happened (ie bids/offers that have been displayed but nobody cared on).

You could start with a simple equation.

P(getting hit) * volume when I get hit * edge to the bid_price= volume when I lift * edge to the ask_price

You can solve for P(getting hit) to find a breakeven for how often you’d need to get hit to compensate you for not lifting.

While this is stylized and simple it’s not an attempt to point to some abstract HFT optimization problem. It’s a reminder that reflecting on your execution techniques sharpens your thinking about trading, conditional edge, adverse selection. It’s less important for retail or if you don’t transact often, but for professionals and asset managers it is justifiably top-of-mind.

“A sale is made on EVERY call”

Remember Ben Affleck in Boiler Room:

And there is no such thing as a no-sale call. A sale is made on every call you make. Either you sell the client some stock or he sells you a reason he can't. Either way a sale is made, the only question is who is gonna close? You or him?

Every time you trade with a broker someone gets the best of it. If you consistently get allocations for 60 contracts when you should have gotten 70 you are destroying 14% of your annual profit. Specialists and DMMs had rules about allocation quantities but there were also unwritten rules. You were expected to fight for even a single contract that you are “entitled” to and advocate forcefully for your interests constantly. The pugilism was built right into the training and culture. The stories of ruthlessness were culturally rewarded. As a junior trader, sticking it to a competitor or getting into a nose-to-nose screaming battle with a broker just to define boundaries was a way to earn stripes.

[This is not my native personality but you adopt what it takes. After all, the only point of this job is to make as much money as possible. Sure, the cost likely bore itself as chronic anxiety about work but only the most well-matched people get the luxury of getting paid and being comfortable. I don’t miss all the daily haggling but I did take it seriously since it was one of the most impactful contributions to profit for the reasons above.

One story I had brought to my attention in the past year — a PM who ran one of the large banks deriv desks reminisced about the AMEX when we were in the same pit. He’s a bit younger than me and apparently I made a big scene sticking up for him to a broker who tried to bully him in the pit. Nice to hear even though I don’t remember the exact incident. I do have a vague memory of lots of battles in that pit because it was a large crowd in a very liquid name.]

Final thoughts on this theme: if you manage a business that’s a game of inches, it’s good to periodically check-in and ask “are we clawing for those inches?”

Is everyone at the point-of-sale aware of what needs to be done or are we getting sloppy? Are we leaking info? Are we too nice? Would it pay to be squeakier? Are we paying the brokers we want to be paying? Are we paying the brokers the right amount?

Evergreen:

Stay Groovy

☮️

Moontower Weekly Recap

Need help analyzing a business, investment or career decision?

Book a call with me.

It's $500 for 60 minutes. Let's work through your problem together. If you're not satisfied, you get a refund.

Let me know what you want to discuss and I’ll give you a straight answer on whether I can be helpful before we chat.

I started doing these in early 2022 by accident via inbound inquiries from readers. So I hung out a shingle through the Substack Meetings beta. You can see how I’ve helped others:

Moontower On The Web

📡All Moontower Meta Blog Posts

👤About Me

Specific Moontower Projects

🧀MoontowerMoney

👽MoontowerQuant

🌟Affirmations and North Stars

🧠Moontower Brain-Plug In

Curations

✒️Moontower’s Favorite Posts By Others

🔖Guides To Reading I Enjoyed

🛋️Investment Blogs I Read

📚Book Ideas for Kids

Fun

🎙️Moontower Music

🍸Moontower Cocktails

🎲Moontower Boardgaming

After reading Zvi's post, I was really disappointed to hear the Economist's podcast on the topic this week. Freedom, yes, but so little discussion of their selection/exclusion efforts. There was mention of a Betfair peer market which is a better design at least. The futures style being promoted by Kalshi is much better.

This newsletter was 🔥

I particularly enjoyed the market making stories, but the gambling thing is serious. I was shocked to see how endemic it was amongst young males. In my youth, I spent my time, brain cells and money mostly on stupid things but at least they gave me a remote chance to get *lucky* (i don't see that happening with betting)